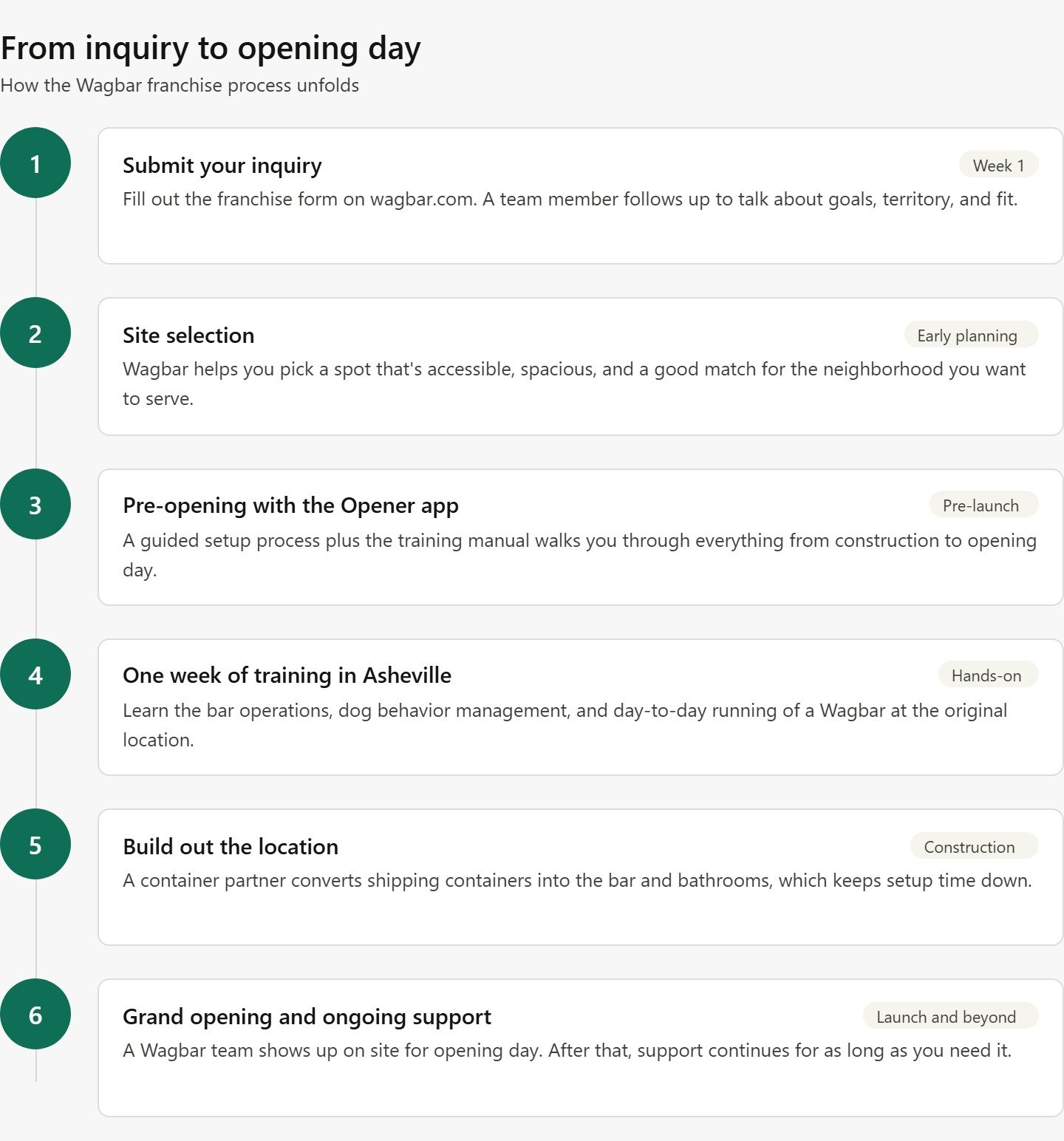

Using a ROBS to Fund Your Dog Franchise Without Taking on Debt

Key Takeaways

A ROBS, or Rollover for Business Startups, lets you use existing 401(k) or IRA funds to capitalize a dog franchise without triggering early withdrawal taxes or penalties and without taking on debt. The structure is legal when set up correctly and is used by more than half of all franchise buyers. If you have $50,000 or more in retirement savings, talk to a qualified ROBS provider before assuming a loan is your only option.

Most people looking at a dog franchise opportunity like Wagbar assume they need a bank loan. The numbers — a total investment range of $470,300 to $1,145,900 and a $50,000 franchise fee* — can feel like they require outside financing by default. But a significant share of franchise buyers fund part or all of their investment without borrowing a dollar.

The mechanism is called a ROBS: Rollover for Business Startups. It's not a loan. It's not a withdrawal. It's a legal structure that allows you to use money sitting in a 401(k) or IRA to fund a business without paying early withdrawal penalties or income taxes on the amount you use. According to Guidant Financial's 2024 Small Business Trends survey, more than 50% of franchise business owners reported using ROBS, and roughly 40% of all ROBS transactions are tied to franchise purchases specifically.

Understanding how the structure works — and where it can go wrong — is worth doing before you approach a lender or sign anything.

What a ROBS Actually Is

A ROBS is not a tax dodge. It's a federally recognized financing structure that the IRS has explicitly addressed in guidance, specifically through its 2010 Memo on Employee Plans Compliance Resolution System. When structured and administered correctly, it is entirely legal. When structured poorly or left without proper ongoing administration, it can trigger an IRS audit and significant tax consequences.

The basic concept: your retirement funds are allowed to invest in a private company under ERISA rules that govern qualified retirement plans. A ROBS applies that principle to your own business by creating a corporate structure that satisfies IRS and Department of Labor requirements for the investment to be permissible.

What it is not: a taxable distribution. When you take money out of a 401(k) early — before age 59½ — you normally pay income tax on the full amount plus a 10% early withdrawal penalty. A ROBS avoids both of those costs entirely, because the money is never actually withdrawn. It's moved from one qualified plan into another and invested into your new business's stock. You don't get a 1099-R. You don't owe taxes at closing.

How the ROBS Structure Works Step by Step

The process has four core steps, and the order matters:

Step 1: Form a C-corporation. ROBS requires a C-corp, not an LLC or S-corp. This is because the structure involves a retirement plan purchasing stock in the company, and only C-corps issue the type of qualifying employer securities that qualified plans can hold. Franchisees who prefer a different operating structure often maintain the C-corp as the holding entity and operate through a subsidiary — a detail a qualified attorney or ROBS provider can help structure properly.

Step 2: Establish a new qualified retirement plan. The C-corp sponsors a new 401(k) plan. This is a real, ongoing retirement plan — not a shell. It has to be administered as such going forward, which is part of the annual compliance work ROBS providers handle.

Step 3: Roll over your existing retirement funds. You roll your existing 401(k) or IRA into the new company's retirement plan as a tax-free, penalty-free rollover. The IRS recognizes rollovers between qualified plans as non-taxable events. The money moves without triggering any tax consequences.

Step 4: The retirement plan purchases stock in the C-corp. The new 401(k) plan uses the rolled-over funds to buy stock in the C-corporation. The corporation now has capital — your capital — to use for business expenses including the franchise fee, build-out, equipment, and working capital. You own the business. Your retirement plan owns stock in the business. Understanding the full scope of starting an off-leash dog bar business helps clarify exactly which cost categories the rolled-over funds need to cover.

The entire setup typically takes two to four weeks from engagement to funded, which is significantly faster than the 60–90 day SBA loan process.

Why ROBS Works Particularly Well for Franchise Businesses

Franchises are one of the cleaner use cases for ROBS, for a few reasons.

First, franchisors like Wagbar require franchisees to demonstrate financial qualification. Having retirement funds available and being able to deploy them quickly as equity — rather than waiting for loan approval — can accelerate the timeline from signed FDD to open location. You can review the full Wagbar franchising model and investment details to understand what financial qualification looks like in practice.

Second, the franchise system provides the business infrastructure that lenders and the IRS both want to see. You're not building a business concept from scratch; you're operating under a proven system with documented training, support, and a brand. That context matters when a ROBS provider reviews your situation, because the structure works best when there's a credible business plan behind it.

Third, ROBS can be combined with SBA financing. Many franchisees use ROBS to cover the equity injection requirement on an SBA loan — using retirement funds for the 10–30% down payment while borrowing the remainder. This combination gives franchisees access to more capital than ROBS alone might provide while avoiding the taxes and penalties of a traditional early withdrawal. For a deeper look at how those two financing tools work together, the SBA 7(a) vs. 504 loan guide for dog franchise investors covers the mechanics of combining funding sources.

Applying ROBS to a Wagbar Franchise Investment

Wagbar's total investment range of $470,300 to $1,145,900* spans a wide spread depending on market, site conditions, and build-out requirements. A ROBS can cover some or all of that range depending on the size of the retirement account being rolled over.

Someone with $200,000 in a 401(k) could use those funds to cover the $50,000 franchise fee, a portion of the build-out, initial equipment, and working capital reserves — while financing the remainder through an SBA 7(a) loan. Someone with $600,000 or more in retirement savings could potentially fund an entire lower-range Wagbar investment without borrowing at all.

The practical floor most ROBS providers work with is $50,000 in eligible retirement savings. Below that threshold, the setup costs and compliance overhead make the structure less efficient relative to other financing options. Most providers also want to see funds in a 401(k) or traditional IRA — Roth IRAs are generally not eligible because their basis has already been taxed and the structure creates complications.

Because owning a pet franchise involves ongoing royalty obligations — Wagbar's royalty is 6% of adjusted gross sales plus a 1% marketing fund contribution* — keeping your first months of operating capital free of debt service can meaningfully affect how quickly a location reaches positive cash flow. Reviewing dog franchise profit margins and real owner financial stories alongside your ROBS planning gives you a realistic model for how that cash flow timing plays out.

The Real Risks You Need to Understand

ROBS is legal, but that doesn't mean it's without risk. Anyone considering this structure should have a clear-eyed view of what can go wrong.

Your retirement savings are at risk. When your 401(k) invests in your business, it holds stock in that business. If the business fails, the stock loses value. Unlike a diversified retirement portfolio, there's no hedge. People who've used ROBS and seen their business struggle have, in some cases, lost the retirement savings they rolled over. Understanding the revenue streams available to an off-leash dog bar — memberships, day passes, bar sales, events — and how they combine to support debt service and operating costs helps you assess this risk honestly before committing.

C-corporation compliance adds complexity. Operating as a C-corp means dealing with double taxation on dividends (the corporation pays corporate income tax; shareholders pay tax again on distributions), annual corporate minutes, separate filings, and stricter administrative requirements than an LLC. Many franchisees handle this by working with an accountant familiar with ROBS structures.

The retirement plan requires ongoing administration. The 401(k) plan sponsoring your business investment has to function as a real qualified plan — annual non-discrimination testing, Form 5500 filings, and participant disclosures. ROBS providers typically bundle this administration into their annual fee. If you stop paying for administration and the plan lapses, the IRS can retroactively disqualify the structure, creating significant tax liability.

IRS scrutiny is real. The IRS has identified ROBS as a "listed transaction" under review and has audited ROBS users. That doesn't mean valid ROBS structures are invalidated — properly administered arrangements have survived audits — but it does mean documentation, ongoing compliance, and a well-qualified provider are non-negotiable, not optional.

ROBS vs. SBA Loans vs. Personal Cash

Consideration ROBS SBA 7(a) Loan Personal Cash Debt created No Yes No Monthly loan payments No Yes No Tax consequences at funding None if structured correctly None None (post-tax funds) Retirement savings at risk Yes — stock in your business No No Setup cost $3,500–$5,000 + ~$1,500/yr admin Guarantee fees + lender fees None Timeline 2–4 weeks 60–90 days Immediate Amount available Limited to retirement account balance Up to $5M with credit/collateral Limited to liquid savings Ongoing compliance Annual plan administration required Loan covenants and reporting None

The strongest use case for ROBS is a franchisee who has substantial retirement savings, wants to avoid debt service in the early months of operation, and has the risk tolerance to accept that those savings are backing the business. The pet industry market analysis — U.S. pet spending exceeded $147 billion in 2023, with 67% household pet ownership — provides the market context that makes that risk tolerance easier to calibrate. The weakest use case is someone with a small retirement account — under $100,000 — looking to fund a mid-to-large-range franchise investment entirely through ROBS. The math doesn't usually work and the compliance overhead is proportionally high. Reviewing dog business models and their capital requirements helps clarify which investment tier actually fits your available retirement assets.

What to Look for in a ROBS Provider

The provider you choose matters more than most people realize. Because the IRS scrutinizes ROBS arrangements, the quality of the legal and administrative setup directly affects your exposure.

The two most established providers in the franchise space are Guidant Financial — which has facilitated over 25,000 ROBS transactions and deployed more than $4 billion in business financing — and Benetrends Financial, which pioneered the ROBS concept over 40 years ago and reports a 97% SBA loan approval rate for clients who pair ROBS with SBA financing. Both providers have specific experience with franchise transactions and understand how franchise disclosure documents, royalty obligations, and SBA eligibility interact with the ROBS structure.

When evaluating providers, ask:

How many ROBS structures have they set up specifically for franchise investments?

What does ongoing annual administration include, and what does it cost?

Have any of their client arrangements been challenged in IRS audits? What was the outcome?

Do they provide legal review of the corporate documents, or just the plan documents?

What happens to the structure if the business is sold or the franchise agreement expires?

The answers reveal how much the provider understands about the downstream implications — not just the initial setup.

Reviewing what to look for when investing in an off-leash dog bar franchise alongside your ROBS research helps you think through the full investment picture — because the financing decision and the franchise selection decision are connected. Understanding what a franchise actually is and how the FDD governs the relationship between franchisor and franchisee also helps you ask sharper questions when evaluating whether the business model's projected cash flows support the risk your retirement savings are taking on.

Frequently Asked Questions

How much money do I need in retirement savings to use a ROBS?

Most ROBS providers set a practical floor of $50,000 in eligible retirement savings — typically in a 401(k), 403(b), or traditional IRA. Below that amount, the setup costs ($3,500–$5,000) and ongoing administration fees (~$1,500 per year) consume a meaningful percentage of the funds, and the structure becomes less efficient. For a Wagbar investment, most investors using ROBS will roll over $150,000 or more to make the numbers work, either to cover the full equity injection requirement on an SBA loan or to fund a larger portion of the investment independently.

Can I use a Roth IRA for a ROBS?

Generally, no. Roth IRA funds have already been taxed, and the ROBS structure is built around pre-tax retirement accounts. Roth rollovers into a new 401(k) create complications that most providers won't take on. If you have both Roth and traditional retirement accounts, the traditional funds can be used for ROBS while the Roth accounts remain invested separately.

Does using a ROBS affect my ability to get an SBA loan?

No — and the two are frequently combined. ROBS funds used as equity injection for an SBA loan satisfy the SBA's 10% minimum equity requirement. Lenders view ROBS-sourced equity the same way they view personal savings. Benetrends Financial reports a 97% SBA approval rate for clients pairing ROBS with SBA 7(a) loans, suggesting the combination is well understood by SBA lenders experienced in franchise financing.

What happens to the ROBS structure if I sell the franchise?

When the business is sold, the C-corp typically sells its assets or shares. The retirement plan receives proceeds from the sale of its stock. Those proceeds stay in the plan as retirement savings — taxed only when distributed in retirement, the same as any other qualified plan investment. A qualified ROBS provider and tax advisor should be involved in structuring any business sale to ensure the plan's proceeds are handled correctly.

Is a ROBS the right choice if I already have minimal retirement savings?

Probably not as a primary funding source. If you have under $100,000 in eligible retirement savings, using most or all of it to fund a business concentrates your financial risk significantly and leaves little room for the retirement plan's administrative overhead. In that scenario, an SBA loan with a smaller equity injection from personal savings is usually a more prudent structure. The benefits of owning a pet franchise are real, but they're best accessed through a financing structure that doesn't overextend your personal financial safety net. Market selection matters too — cities with the strongest demographics for dog franchise success tend to reach break-even faster, which affects how long your reserves need to last.

Summary

A ROBS lets you fund a dog franchise without debt by rolling retirement savings into your business, with no taxes, no penalties, and no loan payments. For Wagbar's $470,300 to $1,145,900 investment range, ROBS works best with $150,000 or more in a qualified account, used alone or paired with an SBA loan. Choose a provider with franchise experience and treat ongoing plan compliance as non-negotiable.

*This information is not intended as an offer to sell, or the solicitation of an offer to buy, a franchise. Investment figures are provided for informational purposes only. An offer is made only by Franchise Disclosure Document (FDD). Currently, the following states regulate the offer and sale of franchises: California, Hawaii, Illinois, Indiana, Maryland, Michigan, Minnesota, New York, North Dakota, Oregon, Rhode Island, South Dakota, Virginia, Washington, and Wisconsin. Wagbar Franchising LLC, (828) 554-1021, 7 Kent Place, Asheville, NC 28804.