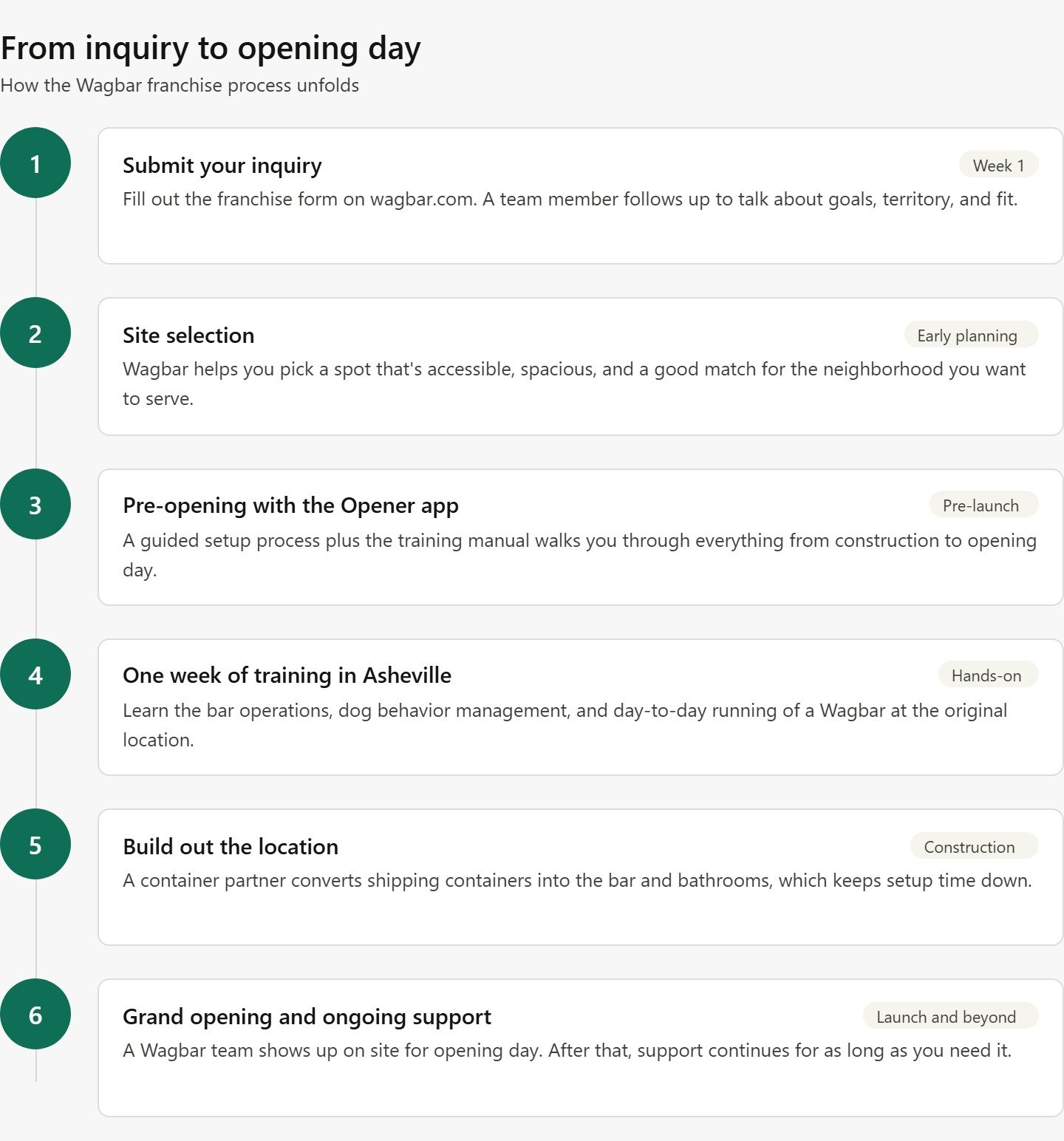

Pet Bar Franchise Royalty Fees Explained: How 6% of Adjusted Gross Sales Is Calculated

Top TLDR: Pet Bar Franchise Royalty Fees at Wagbar run 6% of adjusted gross sales, paid on the cadence defined in the franchise agreement. Adjusted gross sales is gross revenue minus sales tax, refunds, and a short list of specified exclusions, not net profit. Alongside the 1% marketing fund contribution, franchisees pay 7% of adjusted gross sales to the franchisor. Read the Item 6 fee table in the FDD before modeling any unit economics.

Royalty fees are one of the most scrutinized line items during franchise due diligence, and also one of the most misunderstood. The 6% Wagbar collects on adjusted gross sales is not taken from profit, it is taken from top-line revenue, and the precise definition of "adjusted gross sales" determines what counts and what does not. This page breaks down what the royalty actually covers, how it is calculated week by week, how it compares to industry norms, and how it shows up on a pet bar franchise profit and loss statement.

What a Franchise Royalty Fee Actually Is

A royalty fee is the ongoing payment a franchisee makes to the franchisor in exchange for continued use of the brand, operating system, and support infrastructure. It is separate from the one-time franchise fee paid at signing, and separate from the marketing fund contribution that funds brand-level promotion. The royalty is the price of staying in the system after the doors open.

Royalties fund the franchisor's continuing obligations to the operator: ongoing training updates, technology support, operating procedure refreshes, quarterly business reviews, site-support calls, and the back-office teams that handle real estate, compliance, and vendor relationships. In a healthy franchise system, the royalty flowing in funds the support flowing out, and both franchisor and franchisee have direct incentives for the unit to grow revenue.

For Wagbar, the royalty is 6% of adjusted gross sales, collected on the cadence specified in the franchise agreement (typically weekly or monthly depending on the version of the agreement). That 6% sits inside the broader pet bar franchise financials picture, alongside the $50,000 franchise fee, the 1% marketing fund contribution, and the $470,300 to $1,145,900* total initial investment range.

This information is not intended as an offer to sell, or the solicitation of an offer to buy, a franchise. It is for information purposes only. An offer is made only by Franchise Disclosure Document.

Where the 6% Royalty Sits in the FDD

Item 6 of the Franchise Disclosure Document is the section that lists all recurring fees a franchisee pays. The royalty, the marketing fund contribution, and any other ongoing fees show up in a standardized table with the amount, the due date, and the remarks column explaining what the fee covers.

Item 5 of the FDD covers initial fees (franchise fee, training costs paid to the franchisor, any initial inventory or technology fees). Item 6 covers ongoing fees. Item 11 describes the franchisor's pre-opening obligations, including what the royalty helps fund on an ongoing basis. Reading these three items together gives a complete picture of what money flows from franchisee to franchisor and what the franchisee gets in return.

Anyone evaluating the Wagbar royalty in isolation without reading Items 5, 6, and 11 is missing context. The complete guide to what a franchise is walks through the 23 FDD items and the weight each carries during due diligence.

How "Adjusted Gross Sales" Gets Defined

The royalty is 6% of adjusted gross sales, and "adjusted gross sales" is a defined term in the franchise agreement. The exact definition is in Item 6 of the FDD and in the franchise agreement itself, and it is the single most important paragraph to read carefully during due diligence because it controls what gets included in the royalty base.

In most franchise agreements for hospitality-plus-membership concepts, adjusted gross sales typically means:

Gross revenue from all sources at the location, including memberships, day passes, bar sales, food sales (when applicable), private event rentals, merchandise, and any programmed event revenue.

Minus sales tax actually collected and remitted to tax authorities. Sales tax is not revenue to the business; it is money the business collects on behalf of the state and passes through. Deducting it from the royalty base makes economic sense because royalties should be paid on actual business revenue, not on pass-through amounts.

Minus refunds and chargebacks that are actually issued. A canceled membership that is refunded within the refund window is deducted from the royalty base because no revenue was finally earned.

Minus specific exclusions listed in the franchise agreement. These vary by concept but commonly include things like gift card sales (which are recognized when redeemed, not sold), promotional credits not funded by real revenue, and certain reimbursements.

The definition does not typically subtract cost of goods sold, payroll, rent, or any operating expense. That is the key point: royalties are paid on top-line revenue minus specific exclusions, not on profit. For the full picture of how top-line revenue is built from the four main streams, the revenue streams guide for off-leash dog bars walks through membership, day pass, bar, and event revenue.

A Week-by-Week Calculation Example

The easiest way to see how the 6% works is to run a sample week.

Imagine a mid-size Wagbar location in its second operating year. Gross revenue for the week breaks down as follows:

Membership sales (new signups and renewals): $4,200

Day passes: $1,800

Bar sales: $11,500

Private event deposit: $750

Merchandise: $250

Total gross revenue: $18,500

From that $18,500, sales tax of approximately $920 was collected and will be remitted to the state. Two membership refunds totaling $120 were processed during the week. Adjusted gross sales for the week is:

$18,500 minus $920 (sales tax) minus $120 (refunds) = $17,460 in adjusted gross sales

The 6% royalty on that week's adjusted gross sales:

$17,460 × 0.06 = $1,047.60 royalty

The 1% marketing fund contribution on the same base:

$17,460 × 0.01 = $174.60 marketing fund

Total franchisor payment for the week: $1,222.20 (7% of adjusted gross sales).

Over a year at that pace, a location running $900,000 in annual gross revenue with typical sales tax and refund adjustments would pay roughly $51,000 to $52,000 in royalties and $8,500 to $8,700 in marketing fund contributions, depending on the exact tax rate and refund volume. For more on the operating model these royalty payments fund, the off-leash dog bar concept page walks through the experience the system supports.

How the Royalty Compares to Industry Norms

Royalty rates across the pet franchise industry generally run between 5% and 9% of gross or adjusted gross sales, with 6% sitting in the middle of that range. Hospitality and bar concepts commonly fall at the higher end because of the operating complexity; service-only concepts (dog grooming, dog training) sometimes fall at the lower end. Membership-heavy concepts vary widely based on how the membership revenue is structured.

A 6% royalty combined with a 1% marketing fund produces a 7% total ongoing contribution to the franchisor, which is in the normal range for an integrated hospitality-plus-membership concept. The pet industry franchises overview gives a broader view of where different categories land on royalty rates.

What matters more than the headline royalty rate is what the franchisee gets for that fee. A 6% royalty paid to a franchisor with strong ongoing support, active territory protection, regular training updates, and continued technology investment produces very different value than a 6% royalty paid to a franchisor with minimal continuing obligations. During due diligence, buyers who call franchisees from Item 20 of the FDD are really asking two questions: is the support good, and is the royalty earning its keep?

How the Royalty Shows Up on a Franchisee's P&L

On the operating statement, royalties appear as an operating expense line just below revenue and cost of goods sold, in the same general area as rent and insurance. On a location running $900,000 in annual adjusted gross sales, the royalty and marketing fund combined consume roughly $60,000 to $65,000 per year, sitting alongside:

Rent and common area maintenance: typically 7% to 12% of revenue

Payroll: typically 25% to 35% of revenue

Cost of goods sold (bar): roughly 22% to 28% of beverage revenue

Insurance, utilities, technology, marketing spend: additional 10% to 15% of revenue combined

The gap between gross revenue and cash flow is where first-year surprises tend to live. A location that plans well for rent and payroll but underestimates royalty and marketing fund contributions can end up drawing down working capital faster than planned. The dog business franchise profit margins and owner stories page shows how operating margins actually play out once all the fixed lines are accounted for.

Reporting, Payment, and Audit Rights

The franchise agreement specifies how and when royalties are reported and paid. Most agreements require:

Weekly or monthly reporting of adjusted gross sales through the point-of-sale system the franchisor has integrated with its back-office reporting. This integration removes the need for manual reporting and reduces the risk of reporting errors.

Automatic payment via ACH debit on a defined schedule. Most agreements authorize the franchisor to draft royalty and marketing fund payments directly from the franchisee's operating account on the same cadence as reporting.

Record-keeping obligations that require the franchisee to maintain sales records, bank statements, and tax filings for a specified period (typically three to seven years) so the franchisor can audit the calculation if needed.

Audit rights that allow the franchisor to inspect franchisee records periodically to confirm royalty payments are accurate. Most audits result in no adjustment; occasional audits find underreporting (usually from misclassified exclusions), and the franchise agreement specifies how underpayments get trued up and who pays the audit cost if a material variance is found.

The pet business legal guide on licensing, insurance, and compliance covers the broader record-keeping and compliance obligations franchisees assume alongside the royalty reporting requirement.

Why the Royalty Rate Is Not Negotiable

A question that comes up regularly during due diligence: can the royalty be negotiated? For most established franchise systems, including Wagbar, the answer is no. Franchise systems maintain uniform economic terms across all franchisees as a matter of fairness and legal protection. If one franchisee negotiated a 5% royalty while others paid 6%, the system would face immediate disclosure obligations to every other franchisee and risk claims of discriminatory treatment.

What can sometimes vary by negotiation: territory size, multi-unit development commitments (which can trigger the 50% franchise fee discount at three or more units), and specific site approval timelines. The royalty rate itself is held constant to protect the system's operating economics and to keep the franchisee base aligned. The benefits of owning a pet franchise walks through why system uniformity actually benefits individual franchisees over time.

How the Royalty Changes With Multi-Unit Development

The royalty rate does not change based on the number of units an operator runs. A single-unit operator pays 6% of adjusted gross sales, and a three-unit operator pays 6% of adjusted gross sales at each location.

What does change at scale: back-office efficiency. A multi-unit operator can share accounting, HR, area management, and marketing resources across locations, which reduces the per-unit overhead burden. The 6% royalty stays constant, but other operating expenses decline on a per-unit basis. That is part of why experienced franchisees often build toward multi-unit portfolios. The complete guide to starting an off-leash dog bar business covers how operating economics shift across single-unit, two-unit, and three-plus-unit configurations.

Frequently Asked Questions

Is the royalty calculated on gross revenue or net profit?

On adjusted gross sales, which is gross revenue minus sales tax, refunds, and specific exclusions listed in the franchise agreement. It is not calculated on net profit. Operating expenses like rent, payroll, and cost of goods sold are not subtracted before the royalty is calculated.

What is the Wagbar royalty rate?

6% of adjusted gross sales. A separate 1% of adjusted gross sales goes to the brand marketing fund, for a combined 7% contribution to the franchisor on ongoing revenue.

When are royalties paid?

The cadence is defined in the franchise agreement, typically weekly or monthly. Most agreements authorize automatic ACH debit from the franchisee's operating account on the defined schedule, so there is no manual payment step.

Is sales tax included in the royalty calculation?

No. Sales tax collected from customers and remitted to state tax authorities is excluded from adjusted gross sales. Royalties are paid on actual business revenue, not on pass-through amounts.

Are gift card sales included?

Gift card accounting varies by franchise agreement, but a common treatment excludes the sale of a gift card from adjusted gross sales and includes the redemption when the gift card is used to purchase goods or services. Review the franchise agreement definition for the exact treatment.

Can the royalty rate be negotiated?

No. Wagbar, like most established franchise systems, maintains uniform royalty terms across all franchisees. What can vary: territory size, multi-unit development commitments (which trigger a 50% franchise fee discount at three or more units), and specific site approval timelines.

How does the royalty compare to other pet franchises?

Royalty rates across the pet franchise industry range from 5% to 9% of gross or adjusted gross sales. The 6% Wagbar rate sits in the middle of that range, which is normal for an integrated hospitality-plus-membership concept. The Wagbar franchising page lists the full fee structure, including the franchise fee and multi-unit discount mechanics.

What does the 1% marketing fund cover?

The 1% marketing fund contribution is pooled across the system and spent on national brand-building, creative asset development, and digital infrastructure that individual locations use. It is separate from local marketing, which each franchisee funds directly.

What if I dispute a royalty calculation?

The franchise agreement specifies a dispute resolution process. Most royalty disputes are resolved through reconciliation against point-of-sale reports and bank records. If a material variance is confirmed, the agreement specifies how underpayments or overpayments are trued up.

Summary

Bottom TLDR: Pet Bar Franchise Royalty Fees at Wagbar equal 6% of adjusted gross sales (gross revenue minus sales tax, refunds, and specified exclusions), paid on the cadence set in the franchise agreement. The 1% marketing fund contribution brings total franchisor payments to 7% of adjusted gross sales. Model these two lines into the operating statement alongside rent, payroll, and cost of goods before the FDD review is complete.

FDD Disclaimer: This information is not intended as an offer to sell, or the solicitation of an offer to buy, a franchise. It is for information purposes only. An offer is made only by Franchise Disclosure Document (FDD). Currently, the following states regulate the offer and sale of franchises: California, Hawaii, Illinois, Indiana, Maryland, Michigan, Minnesota, New York, North Dakota, Oregon, Rhode Island, South Dakota, Virginia, Washington, and Wisconsin. If you are a resident of, or wish to acquire a franchise for a Wagbar to be located in one of these states or a country whose laws regulate the offer and sale of franchises, we will not offer you a franchise unless and until we have complied with applicable pre-sale registration and disclosure requirements in your jurisdiction. Wagbar Franchising LLC, (828) 554-1021, 7 Kent Place, Asheville, NC, 28804.