Pet Bar Franchise Financials and Investment Information

Top TLDR: Pet Bar Franchise Financials for Wagbar start at a $50,000 franchise fee with a total initial investment range of $470,300 to $1,145,900, a 6% royalty on adjusted gross sales, and a 1% marketing fund contribution. A 50% franchise-fee discount applies at three or more committed units. Request the Franchise Disclosure Document before modeling any return on investment.

Buying into a pet bar franchise is a real capital decision, and the numbers behind it deserve a close read long before any paperwork gets signed. This page walks through the Wagbar investment structure the way a prospective franchisee would actually encounter it: the one-time franchise fee, the total project cost, the ongoing royalty and marketing fund, the revenue streams that feed gross receipts, and the financing paths that most buyers use to put the deal together. Wherever a dollar figure appears, it maps to the figures Wagbar publishes in its Franchise Disclosure Document, and the FDD remains the authoritative source for any final decision.

What the Total Investment Range Covers

The total initial investment for a Wagbar pet bar franchise runs from $470,300 on the low end to $1,145,900 on the high end.* That range reflects real differences between markets, not a soft estimate. A mid-size suburban site with reasonable landlord concessions and a container bar build-out will sit closer to the low end. A metro build with premium real estate, longer site preparation, and a full from-the-ground-up bar construction will push toward the high end.

Within that range, the line items that show up consistently in Item 7 of the FDD include the franchise fee, initial training and travel, pre-opening real estate costs (deposits, first months of rent, landlord work letters), site preparation and landscaping for the off-leash area, the bar build-out, fencing, surface treatment, furniture, point-of-sale and technology systems, initial inventory of beer, wine, and non-alcoholic beverages, signage, opening marketing, licenses and permits, insurance deposits, working capital, and professional fees.

None of these items is unusual for a hospitality concept. The one that catches most buyers off guard is the cost of the dog-specific infrastructure: the fencing standards, drainage, surface material, and shade structures that make an off-leash environment work day after day. A cheaper surface costs less upfront and more in ongoing maintenance and customer complaints. The FDD breaks out which categories are required, which are typical, and which are optional, and interested buyers should walk line-by-line through Item 7 with a financial advisor. The Wagbar franchising overview maps the broader pet bar franchise investment structure alongside Item 7.

This information is not intended as an offer to sell, or the solicitation of an offer to buy, a franchise. It is for information purposes only. An offer is made only by Franchise Disclosure Document (FDD). See the disclaimer at the end of this page for state-specific notices.

The Franchise Fee and How the Multi-Unit Discount Works

The Wagbar initial franchise fee is $50,000 per unit. That fee covers the right to operate under the Wagbar brand, access to the system's operating manual and proprietary Opener pre-opening app, the one-week on-site training program in Asheville, grand opening support, and ongoing use of the brand's marks and operating system.

For buyers who commit to three or more units, Wagbar applies a 50% multi-unit discount on the franchise fee. The mechanics are straightforward: the first three committed units effectively move from a combined $150,000 in fees to $75,000, a $75,000 difference that can be redirected into working capital, marketing, or build-out upgrades. The discount is tied to the area development agreement, which also sets development milestones (a schedule for when each unit must open) and a defined territory the operator controls during the build-out phase.

Multi-unit development changes the math on more than just the franchise fee. A second or third location shares back-office costs with the first, allows a general manager structure to become economically viable, and often warrants stronger lender terms because the borrower is treated as a developing operator rather than a single-unit applicant. The 50% fee discount is the visible benefit, but the operating efficiency gained at two or three units is usually a larger win over time.

For buyers starting with a single unit, the option to convert to a multi-unit agreement later is worth discussing with the franchise team before the first deal closes, since some of the structural benefits (territory protection, development rights) work better when committed to up front. The off-leash dog bar concept page explains the operating model these fees fund.

Royalty Fees and the Marketing Fund Contribution

Ongoing fees at Wagbar run in two lines on the profit and loss statement. The royalty is 6% of adjusted gross sales, and the marketing fund contribution is 1% of adjusted gross sales. Together, 7% of adjusted gross sales is paid to the franchisor each period.

"Adjusted gross sales" is defined in the franchise agreement and typically means gross revenue net of sales tax, refunds, and a handful of specified exclusions. Buyers should read the definition carefully in the FDD, because small differences in what counts as adjusted gross sales can translate into meaningful dollars over the life of a location. The royalty covers ongoing brand rights, training updates, technology support, operating procedure refreshes, quarterly business reviews, and the franchisor's back-office resources. The marketing fund is pooled across the system and spent on national brand-building, creative assets, and digital infrastructure that individual locations can plug into.

In the context of the pet franchise industry, a combined 7% royalty-plus-marketing contribution sits in the middle of the typical range. Concepts in the same broad space commonly run between 5% and 9% on royalties alone, with separate marketing contributions layered on top. For a deeper look at how royalty structures affect unit economics across different pet concepts, the revenue streams guide for off-leash dog bars walks through the full P&L implications.

Royalty payments are generally due on a weekly or monthly cadence depending on the franchise agreement. The franchise agreement, which is Item 22 of the FDD, specifies the exact timing, reporting requirements, and any late-payment terms.

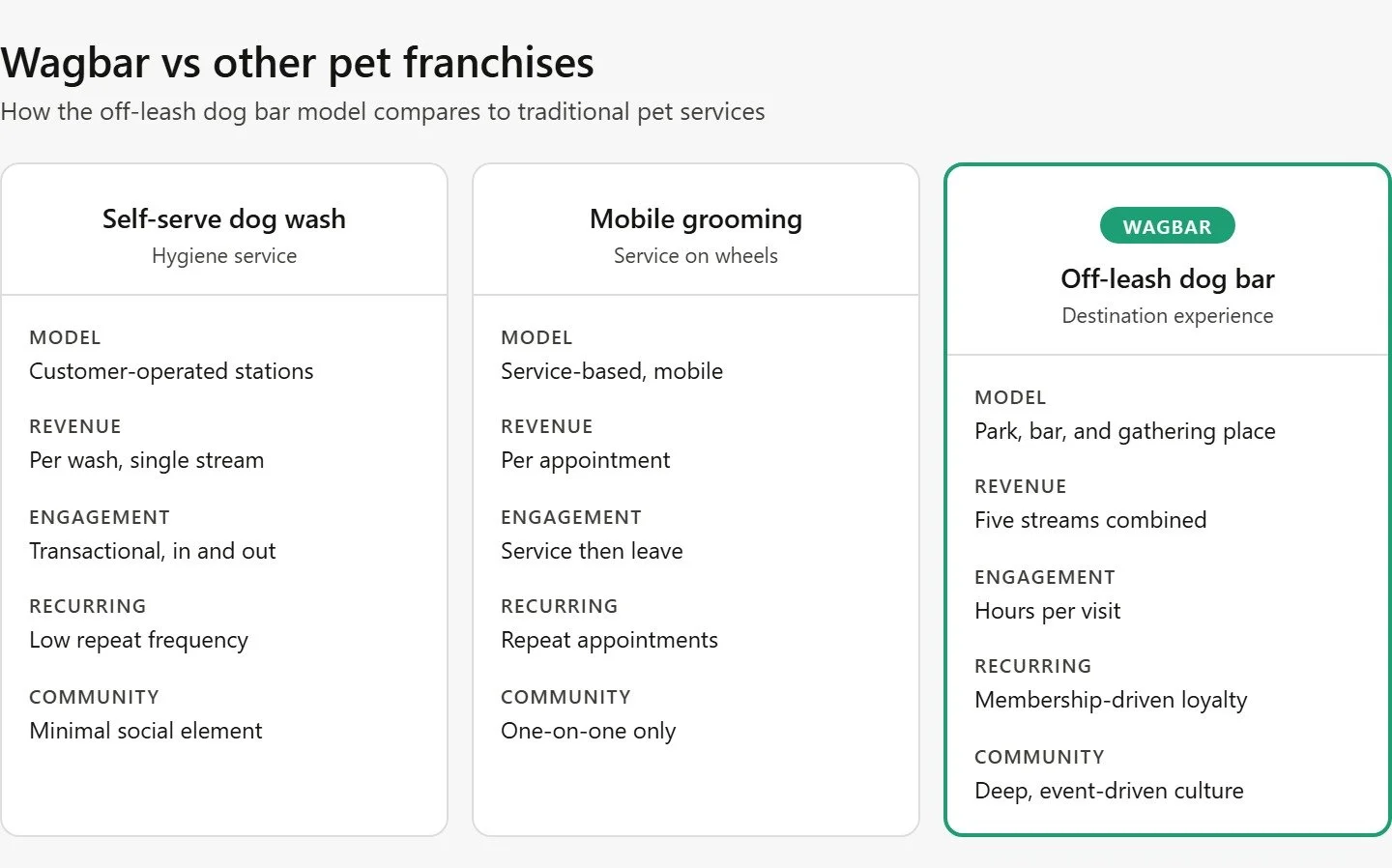

Revenue Streams That Drive Gross Receipts at a Pet Bar

The revenue side of a pet bar franchise is where the economic model diverges from a traditional bar. Gross receipts at a Wagbar location are built from four primary streams, each with a different margin profile and a different operational demand.

Memberships are the anchor stream. Wagbar sells daily passes, monthly memberships, annual memberships, and 10-visit punch passes. Memberships are for dogs only; human entry is always free for guests 18 and over. The annual membership produces the highest lifetime value per customer because it eliminates re-enrollment friction and generates a concentrated upfront revenue event. The monthly tier provides recurring revenue and works well as a conversion pipeline for day-pass visitors.

Bar sales are the highest-margin stream. Members visit more often than day-pass buyers, which means membership retention directly drives bar revenue. An active annual member visiting two or three times a week contributes more in bar sales over twelve months than the membership fee alone. The bar is where gross margin lives; memberships are what keep customers walking back through the door.

Private events and space rentals add incremental revenue that does not compete with regular operations. Some Wagbar locations host birthday parties, corporate gatherings, breed-specific meetups, and adoption events. Event revenue typically carries higher per-visit spending than a standard afternoon visit.

Merchandise, food truck revenue share, and programmed events round out the mix. Food truck partnerships can generate a percentage of sales without the operating complexity of running a kitchen. Programmed events (trivia, live music, themed nights) drive traffic on historically slower days and lift both bar revenue and membership sign-ups at the point of sale.

Understanding how these four streams interact is the real financial planning work. A location that over-indexes on day passes and under-indexes on memberships will show strong summer weekends and weak weekday revenue. A location with a deep annual member base will show steadier week-over-week revenue and higher bar contribution margin. For a structured look at the dog business franchise profit margins and owner stories that map to these streams, the owner-perspective breakdown is worth reviewing during due diligence.

How FDD Item 19 Frames Financial Performance

Item 19 of the Franchise Disclosure Document is the section most prospective franchisees want to see first. It is also the section that requires the most careful reading.

Federal franchise law does not require a franchisor to include any financial performance representations in Item 19. A franchisor can choose to publish actual results from franchised or company-owned units, publish nothing, or publish a limited subset. If a franchisor publishes nothing in Item 19, salespeople are legally prohibited from making any earnings claims whatsoever, verbally or in writing. That is a protection for the buyer, not an absence of information.

When Item 19 does contain data, a few reading rules matter more than the averages themselves. Sample size first: an average drawn from 20 units is more reliable than an average drawn from three. Distribution second: the percentage of units above and below the median tells you whether the average is being pulled by a handful of outliers. Exclusions third: newly opened units (typically less than 12 months of operation) are often excluded, and affiliate-owned units may or may not be included depending on how the disclosure is structured.

Revenue is not profit. A gross revenue figure tells you what came in the door; it does not account for royalties, rent, payroll, cost of goods, utilities, or insurance. A realistic pro forma uses the Item 19 gross-revenue data as a starting point, then layers Item 7 cost estimates, market-specific real estate and wage data, and the royalty and marketing fund structure from Item 6. That work is best done with an accountant who has read franchise financials before.

For a full walkthrough of how Item 19 fits into the rest of the disclosure, the complete guide to what is a franchise covers the 23-item FDD structure and the five items that carry the most weight in a serious financial review.

Working Capital and Liquid Capital Expectations

Working capital is the cash a business needs to cover operating expenses during the ramp period, before revenue is sufficient to cover its own overhead. For a pet bar franchise, the working capital line in Item 7 accounts for the months between opening day and the point where weekly revenue reliably clears operating costs.

Realistic ramp periods for a hospitality-plus-membership concept run three to six months for most markets and longer in slower-climate or lower-population areas. A conservative budget allocates working capital equal to four to six months of fixed operating costs, covering rent, payroll, utilities, insurance, and loan service. Underfunding working capital is the most common reason well-located independent bars struggle in their first year, and it is one of the areas where the franchise system adds real protection: opening pro formas from the franchisor build in working capital assumptions grounded in actual operating history across the system.

Separate from working capital is liquid capital, which is the cash and near-cash reserves the franchisor wants to see on a candidate's personal balance sheet before awarding a franchise. Liquid capital demonstrates that the buyer can fund the equity injection on an SBA loan, cover unexpected opening cost overruns, and weather a slower-than-expected ramp without the business starving itself. Wagbar publishes its specific liquid capital expectations in the FDD and discusses them directly during the candidate review process. As a general rule of thumb across the franchise industry, liquid capital requirements commonly land in the range of 15% to 25% of the total project cost.

For buyers thinking about how their personal balance sheet translates into franchise qualification, the supporting piece on owning a pet franchise covers the personal financial readiness side of the process.

Real Estate, Build-Out, and the Container Bar Option

Real estate and build-out together account for the widest dollar swing inside the $470,300 to $1,145,900* investment range. Two sites with identical square footage can differ by $300,000 or more in total cost depending on landlord concessions, existing infrastructure, permitting timeline, and local construction wages.

A Wagbar location needs two functional zones: a fenced off-leash area with proper drainage and surface, and a bar with food-and-beverage service capacity. The off-leash area is where site selection decisions get technical. Slope, soil type, drainage patterns, shade, and fencing regulations all influence build cost. Municipal zoning requirements for outdoor dog-use facilities vary widely across jurisdictions, and the zoning and regulations guide for pet businesses by state and city covers the compliance layer franchisees work through during site approval.

For the bar itself, Wagbar offers a container bar build-out option as a near-turnkey solution. Wagbar has partnered with a company that converts shipping containers into fully equipped bars and bathroom facilities, which reduces build time, compresses the pre-opening period, and lowers the risk of cost overruns that often hit ground-up bar construction. The container option is not the only path; franchisees can pursue a traditional fixed build when the site and market call for it, and the FDD breaks out the estimated cost differential between the two approaches.

Landlord work letters, tenant improvement allowances, and free rent periods can move the total cost materially. A strong retail broker who understands both restaurant and pet-use requirements is worth the commission, because a well-negotiated lease can return $100,000 or more in effective cost reduction across the first five years of a location.

This information is not intended as an offer to sell, or the solicitation of an offer to buy, a franchise. See the FDD disclaimer at the end of this page.

Financing Paths for a Pet Bar Franchise

Most Wagbar franchisees do not write a check for the full investment. The common financing paths combine personal equity with one or more of three structures: SBA-backed lending, ROBS retirement-rollover funding, or investor-backed ownership.

SBA 7(a) and 504 Loans

The SBA 7(a) loan is the most flexible option for franchise financing. Loan amounts reach up to $5 million, and the program allows funds to be applied to the franchise fee, equipment, real estate, and working capital within a single loan structure. Repayment terms run up to 10 years for working capital and up to 25 years for real estate. Because the SBA guarantees a portion of the loan, lenders extend credit to borrowers who would not qualify for conventional financing at the same terms.

The SBA 504 program is designed specifically for major fixed-asset purchases: real estate and heavy equipment. A 504 loan is structured as a combination of a conventional bank loan covering roughly 50% of project costs and a Certified Development Company loan covering 40%, with the borrower contributing 10%. The lower down payment and longer repayment terms suit locations where real estate acquisition is a large share of the project budget.

Most Wagbar franchisees working with SBA financing use the 7(a) program because the inclusion of working capital and franchise fees in a single loan matches how the opening budget is actually spent. Personal credit scores of 680 or above are the common threshold, with 700-plus producing more favorable terms. A complete application with a reviewed FDD, business plan, and three years of personal financial history typically moves from submission to funding in 60 to 90 days.

ROBS Retirement-Rollover Funding

ROBS (Rollover for Business Startups) lets an owner use existing retirement funds to capitalize a new business without incurring early-withdrawal penalties or immediate income tax. The structure requires forming a C-corporation, establishing a new 401(k) plan within that entity, rolling over existing retirement funds into the new plan, and then having the retirement plan purchase stock in the C-corp. The corporation now has capital to deploy into the franchise.

The full setup runs two to four weeks when executed by a ROBS provider experienced with franchise transactions, considerably faster than the 60-to-90-day SBA timeline. ROBS can also be combined with an SBA loan: retirement funds serve as the equity injection on a 7(a) loan, which unlocks more total capital than either path alone. The practical floor most ROBS providers work with is approximately $50,000 in eligible retirement savings; below that threshold, setup and compliance costs make the structure less efficient than other options.

Investor-Backed Ownership

Some Wagbar franchisees bring in outside capital through investor-backed ownership structures: a silent partner, an active operating partner, a family office, or a small investment group. These structures vary widely in how they share equity, profit distributions, operational control, and exit rights. The franchise agreement defines which ownership changes require franchisor approval and how those approvals are processed, and most agreements require the franchisor to approve any change above a specific ownership threshold.

Investor-backed structures make sense for operators who have the operational skill and market access to run the business but need outside capital to complete the equity stack. They typically do not work well for passive buyers looking for a hands-off return, because the franchisor's model expects an active operator in the business.

For more on how these financing paths work across pet franchise concepts, the pet industry franchises overview provides additional context on capital requirements across the category.

Ongoing Operating Costs Beyond the Royalty and Marketing Fund

The 7% of adjusted gross sales that goes to royalties and the marketing fund is only one line on the operating statement. A realistic pro forma also accounts for:

Rent and common area maintenance, typically 7% to 12% of revenue in most markets. Payroll, commonly 25% to 35% of revenue for a hospitality concept with multiple shift positions and weekend coverage. Cost of goods sold on the bar side, running roughly 22% to 28% of beverage revenue. Insurance, including general liability, liquor liability, workers' compensation, and property coverage. Utilities, waste management, and cleaning. Technology and point-of-sale subscriptions. Repair and maintenance reserves (especially for outdoor surfaces and fencing). Local marketing spend above and beyond the brand fund contribution.

The gap between gross revenue and cash flow is where most first-year surprises live. Operators who planned their opening with a rent-first mindset, underestimating payroll and utilities, are the ones who end up drawing down working capital faster than planned. The complete guide to starting an off-leash dog bar business covers the full operating cost structure that sits below gross revenue.

How the Numbers Shift With Multi-Unit Development

Multi-unit pet bar franchise economics are not simply three times the single-unit math. The structural shift at two or three locations changes what a business looks like financially in three ways.

First, the 50% franchise-fee discount on units two and three drops the effective franchise fee from $50,000 to $25,000 per additional unit. Across a three-unit development agreement, that is a $50,000 reduction compared to three separate single-unit deals.

Second, back-office costs (accounting, human resources, marketing, area management) can be shared across locations. A single operator managing three units commonly spends less than three times the back-office cost of a single unit. That back-office efficiency compounds over time.

Third, a multi-unit operator builds the kind of operating track record that lenders reward with better terms. Financing a fourth or fifth unit is usually easier than financing the first, because the borrower now has audited multi-year operating history, established vendor relationships, and a demonstrated ability to manage across locations. For buyers thinking seriously about best cities for dog franchise success and market demographics, the multi-unit path often influences which markets make the final list.

The counterpoint: opening three units instead of one also triples the execution risk during the ramp period, and the development schedule in the area development agreement sets deadlines that can become operating pressure. Multi-unit commitments suit experienced operators with strong capital reserves and realistic timelines.

What to Ask Before Signing a Pet Bar Franchise Agreement

A few questions separate a well-prepared buyer from a hopeful one:

How did the low end and high end of the Item 7 investment range compare to actual opening costs for recent franchisees? (Item 20 lists franchisee contact information; calling five or six of them is standard practice during due diligence.)

What is the distribution of unit performance, not just the average, if Item 19 contains financial representations? Averages can be pulled by high performers or weighed down by struggling units. The distribution tells a clearer story.

What is the franchisor's ramp assumption for the first 12 months, and how does that match the working capital line in Item 7?

What real estate support does Wagbar provide during site selection, and what has the franchisor's track record been on approving marginal sites versus holding firm for stronger locations?

How are royalty and marketing fund contributions audited? What reporting cadence does the franchise agreement require?

The FDD contains the answers to most of these questions in writing. Franchisees who have opened their own locations can tell you whether the written answers matched reality. Both sources matter; neither is sufficient alone. For context on the operator side of the deal, the benefits of owning a pet franchise walks through the non-financial factors that tend to separate operators who thrive from those who struggle.

Frequently Asked Questions

What is the total investment range for a Wagbar pet bar franchise?

The total initial investment runs from $470,300 to $1,145,900,* covering the franchise fee, training, real estate costs, build-out, fencing and surface treatment, furniture, technology, inventory, licenses, insurance, and working capital. The specific number for any given location depends on market, site conditions, and whether the operator chooses the container bar build-out or a traditional fixed build.

What is the Wagbar franchise fee?

The initial franchise fee is $50,000 per unit. A 50% multi-unit discount applies when the buyer commits to three or more units in a single area development agreement, reducing the effective fee on additional units.

What royalty does Wagbar charge?

The royalty is 6% of adjusted gross sales, plus a 1% contribution to the brand marketing fund. The combined 7% of adjusted gross sales is paid to the franchisor on the cadence specified in the franchise agreement.

Does Wagbar publish financial performance data in Item 19?

The Franchise Disclosure Document is the authoritative source for what Wagbar publishes in Item 19. Franchisors are not required to include financial performance representations, and the specific content of Item 19 changes from year to year as the disclosure is renewed. Request the current FDD and review Item 19 with an accountant.

Can I finance a Wagbar franchise with an SBA loan?

Yes. SBA 7(a) loans are the most common path for franchise investments in this cost range and can fund the franchise fee, real estate, build-out, equipment, and working capital in a single loan. SBA 504 loans can be used for major real estate or equipment components. Personal credit scores of 680 or above are the typical threshold.

Can I use retirement funds to buy a pet bar franchise?

Yes, through a ROBS (Rollover for Business Startups) structure. A properly structured ROBS lets an owner use existing 401(k) or IRA funds to capitalize the business without early-withdrawal penalties or immediate tax. The setup takes two to four weeks and requires working with a ROBS provider who handles the ongoing compliance requirements.

How does the multi-unit discount work?

Committing to three or more units in a single area development agreement triggers a 50% reduction on the franchise fee for additional units beyond the first. The agreement also sets development milestones for when each unit must open and defines the territory the operator controls during the build-out period.

What liquid capital do I need to qualify as a franchisee?

Liquid capital requirements are disclosed in the FDD and discussed during the candidate review process. As a general industry reference, liquid capital expectations across franchise concepts commonly land in the range of 15% to 25% of total project cost, though Wagbar's specific requirement is published in its disclosure document.

What revenue streams make up a pet bar franchise P&L?

The four primary streams are memberships (daily, monthly, annual, and 10-visit punch passes), bar sales, private events and space rentals, and programmed events with merchandise or food truck revenue share. Memberships drive visit frequency, and bar sales provide the highest gross margin per transaction.

How long is the ramp period before a location is cash-flow positive?

Ramp periods vary by market, season, population density, and local competition. The working capital line in Item 7 is sized to cover the operator through the expected ramp. Most hospitality-plus-membership concepts reach positive cash flow within three to six months, though slower-climate or smaller markets can take longer.

Summary

Bottom TLDR: Pet Bar Franchise Financials at Wagbar combine a $50,000 franchise fee, a total initial investment of $470,300 to $1,145,900, a 6% royalty on adjusted gross sales, and a 1% marketing fund contribution, with a 50% fee discount at three or more committed units. Revenue flows from memberships, bar sales, private events, and programmed events. Request the current FDD and review Item 7, Item 19, and Item 20 with a franchise attorney before signing.

FDD Disclaimer: This information is not intended as an offer to sell, or the solicitation of an offer to buy, a franchise. It is for information purposes only. An offer is made only by Franchise Disclosure Document (FDD). Currently, the following states regulate the offer and sale of franchises: California, Hawaii, Illinois, Indiana, Maryland, Michigan, Minnesota, New York, North Dakota, Oregon, Rhode Island, South Dakota, Virginia, Washington, and Wisconsin. If you are a resident of, or wish to acquire a franchise for a Wagbar to be located in one of these states or a country whose laws regulate the offer and sale of franchises, we will not offer you a franchise unless and until we have complied with applicable pre-sale registration and disclosure requirements in your jurisdiction. Wagbar Franchising LLC, (828) 554-1021, 7 Kent Place, Asheville, NC, 28804.