The Dog Park Bar Industry: Growth, Closures, and What's Actually Working in 2026

Top TLDR: The dog park bar industry has grown from roughly 5 venues in 2016 to an estimated 60-70 locations in 2026, but not every operator survives. Bar K's sudden closure of all three locations in July 2025 showed what happens when overhead outpaces revenue. The models that are working run lean, beverage-focused operations with strong membership retention and active community programming. Check the full industry breakdown below for revenue benchmarks, regional patterns, and what's next.

Ten years ago, the phrase "dog park bar" would have gotten you a confused look. Today it describes a category of business that's reshaping how dog owners socialize, how entrepreneurs think about pet services, and how cities plan for the growing population of urban dog owners who want more than a muddy fenced lot and a water fountain that barely works.

The dog park bar concept is straightforward: combine a fenced, supervised off-leash play area for dogs with a licensed bar serving craft beer, wine, cocktails, and non-alcoholic drinks. Charge dogs for entry through memberships or day passes. Let humans in free. Host events. Build community. Repeat.

What's less straightforward is making it work as a business. The dog park bar industry in 2026 is a category in motion, with new venues opening every month, at least one major operator going under, and a handful of franchise models trying to prove the concept can scale. This is a look at where the industry actually stands right now, what the numbers say, and what separates the operators who are growing from the ones who closed their doors.

How Many Dog Park Bars Are There in the US?

Nobody publishes an official count. There's no trade association, no SIC code specific to "dog park bar," and no industry census. So we built an estimate based on what's publicly trackable.

As of mid-2026, we count approximately 60 to 70 dog park bars operating in the United States. That includes single-location independent operators, multi-unit brands, and franchise locations that have opened their doors to the public. It does not include venues that are in development, under construction, or announced but not yet open.

Here's how that breaks down roughly by type:

Independent single-location operators make up the majority. These are locally owned venues like The Dog Bar in St. Petersburg, FL; HopHounds Brew Pup in Mobile, AL; Unleashed Hounds and Hops in Minneapolis; Barkology in Buffalo; and dozens of others scattered across college towns, mid-size metros, and dog-obsessed neighborhoods. Most opened between 2018 and 2024.

Multi-unit brands include MUTTS Canine Cantina (operating locations in Dallas, Fort Worth, Allen, El Paso, and Austin with 19 total in development), Fetch Park (multiple Atlanta-area locations), Bark Social (Maryland), and Pups Pub (Orlando and Tampa). These brands are scaling through either franchise agreements or corporate expansion.

Franchise models with active expansion include Wagbar, which has 16+ franchise territories sold with two locations currently operating, and MUTTS, which has partnered with Fransmart for nationwide franchise development.

Recently opened venues in 2025 and 2026 include K9 Garden in St. Louis (which took over the former Bar K space), Macie and Milo's Brew Pup in Lexington, SC, BARk House Social in East Austin, and Idaho Pups and Ales in Meridian, ID. New openings are happening at a pace of roughly one to two per month nationally.

For context, the first wave of dog park bars emerged around 2013 to 2016, with MUTTS Canine Cantina (Dallas, 2013), Yard Bar (Austin, 2015), and Bar K (Kansas City, 2018) among the earliest. Wagbar opened its flagship location in Asheville, North Carolina in 2019. The category has roughly doubled since 2020, and the growth rate accelerated noticeably after the pandemic drove pet adoption and outdoor social spending.

The Growth Curve: 2016 to 2026

The timeline of the dog park bar industry tracks almost perfectly with three converging trends in American consumer behavior.

The pet spending boom. Americans spent $158 billion on their pets in 2025, up 3.7% from the prior year, according to the American Pet Products Association's 2026 State of the Industry Report (APPA, 2026). That number is projected to reach $165 billion in 2026. Ninety-five million US households own at least one pet. Dog ownership specifically expanded from 51% to 53% of households in 2025. The money is there, and it's growing.

The experience economy shift. Younger pet owners, especially millennials and Gen Z, increasingly spend on experiences rather than products. They want to bring their dogs along for those experiences rather than leaving them at home. A dog park bar lets them do both: have a social outing and give their dog exercise and socialization at the same time. The same generational cohort that fueled the craft brewery boom is now fueling the dog park bar wave.

The craft beverage infrastructure. The explosion of craft breweries, cideries, and taprooms over the past 15 years created a consumer base that expects quality drinks in casual, non-traditional settings. Dog park bars slot naturally into that expectation. Most serve local craft beer alongside wine, hard seltzer, and cocktails. The beverage program doesn't need to be complicated to work.

Here's a rough timeline of how the category evolved:

2013 to 2016: The pioneers. MUTTS Canine Cantina opens in Dallas (2013). Yard Bar opens in Austin (2015). A handful of independent operators experiment with the model. Most are bootstrapped. Nobody knows what to call them yet.

2017 to 2019: The concept gets a name. Bar K opens on the Kansas City riverfront (2018) with a more ambitious vision: full-service restaurant, large events, multiple revenue streams. Wagbar opens in Weaverville, NC (2019) with a leaner model built around a shipping container bar and 25,000 square feet of outdoor play space. The phrase "dog park bar" enters common use. Media coverage picks up. Livability, FSR Magazine, and USA Today start publishing lists and features.

2020 to 2022: Pandemic acceleration. COVID-19 creates a perfect storm for the category. Pet adoptions surge. Outdoor social venues become preferred over indoor spaces. Dog park bars, which are inherently outdoor and socially distanced, see massive demand. New openings accelerate. Fetch Park expands in Atlanta. Bark Social opens in Maryland. MUTTS begins franchising in earnest.

2023 to 2024: Expansion and pressure. The category grows but faces real-world headwinds. Inflation drives up construction, labor, and lease costs. Some operators who expanded aggressively during the pandemic find that post-pandemic consumer spending has shifted. Bar K, once considered the category leader, faces financial strain including a $298,000 unpaid rent lawsuit at its St. Louis location. MUTTS signs deals for 19 locations. Wagbar sells 16 franchise territories in 15 months.

2025 to 2026: Correction and continued growth. Bar K closes all three locations suddenly in July 2025. Off Leash, a full-service dog park restaurant in Alpharetta, GA, closes after less than six months. Meanwhile, new independent operators keep opening, franchise brands keep expanding, and the category matures. The venues that survive this period will define what the industry looks like for the next decade.

Why Some Dog Park Bars Fail

The Bar K closure is the most instructive case study the industry has produced so far.

Bar K launched in Kansas City in 2018 with a two-acre outdoor dog park on the Berkley Riverfront. The concept was ambitious: a full-service restaurant, event spaces, satellite bars, and a large membership-based park. They expanded to St. Louis and Oklahoma City. They were named one of USA Today's best dog bars in 2024. They raised funding and hired a CEO to scale the brand.

Then, on July 29, 2025, they shut down all three locations with no warning. Employees learned about the closure through an internal app. Members with annual subscriptions received no refunds. The company cited "severe economic challenges" including inflation, labor costs, reduced consumer spending, and location-specific problems. In Kansas City, major construction projects had consumed parking and made the venue difficult to reach.

The pattern that emerges from Bar K and other closures points to a few consistent problems.

Over-investment in food service. Running a full kitchen inside a dog park bar dramatically increases complexity. You need kitchen staff, food safety compliance, inventory management, and equipment maintenance on top of everything required to operate a dog park and a bar. As FSR Magazine reported in April 2025, serving food on premises "complicates operations considerably, which is why many emerging dog bars are opting to only serve beverages and perhaps have rotating food trucks." The venues that avoid full-service kitchens and instead partner with food trucks or allow delivery have significantly lower operating costs and simpler compliance requirements.

Location access and lease costs. Bar K's Kansas City location was on the riverfront, which was appealing aesthetically but created vulnerability when construction disrupted access and parking. The St. Louis location carried a lease that apparently became unsustainable, evidenced by the unpaid rent lawsuit. Dog park bars need space, which means leases can be expensive. And unlike a restaurant that can be tucked into a strip mall, a dog park bar requires specific zoning, adequate lot size, and easy access for people carrying leashes and wrangling excited dogs.

Scaling too fast. Expanding from one location to three in different cities requires systems, capital, and management depth that most startups don't have. Bar K attempted to grow into a multi-city brand while still operating as a startup. They hired a CEO who left within months. Each new market introduced new zoning rules, new landlord relationships, new staff pools, and new customer acquisition costs. The revenue streams that work for off-leash dog bars require local density and repeat customers, which take time to build in each new market.

Membership pricing and retention. Dog park bars that depend heavily on membership revenue need to retain members month after month. When access becomes inconvenient (because of construction, weather, or location problems), members churn. When members churn faster than they're replaced, the business loses its financial floor. Bar K's decision to close without offering refunds to annual members suggests the cash reserves were already gone.

Off Leash in Alpharetta, GA followed a similar trajectory. The concept was described as a "full-service restaurant and bar with a premium dog park." It closed after less than six months. The pattern holds: higher operational complexity plus insufficient local market traction equals unsustainable burn rate.

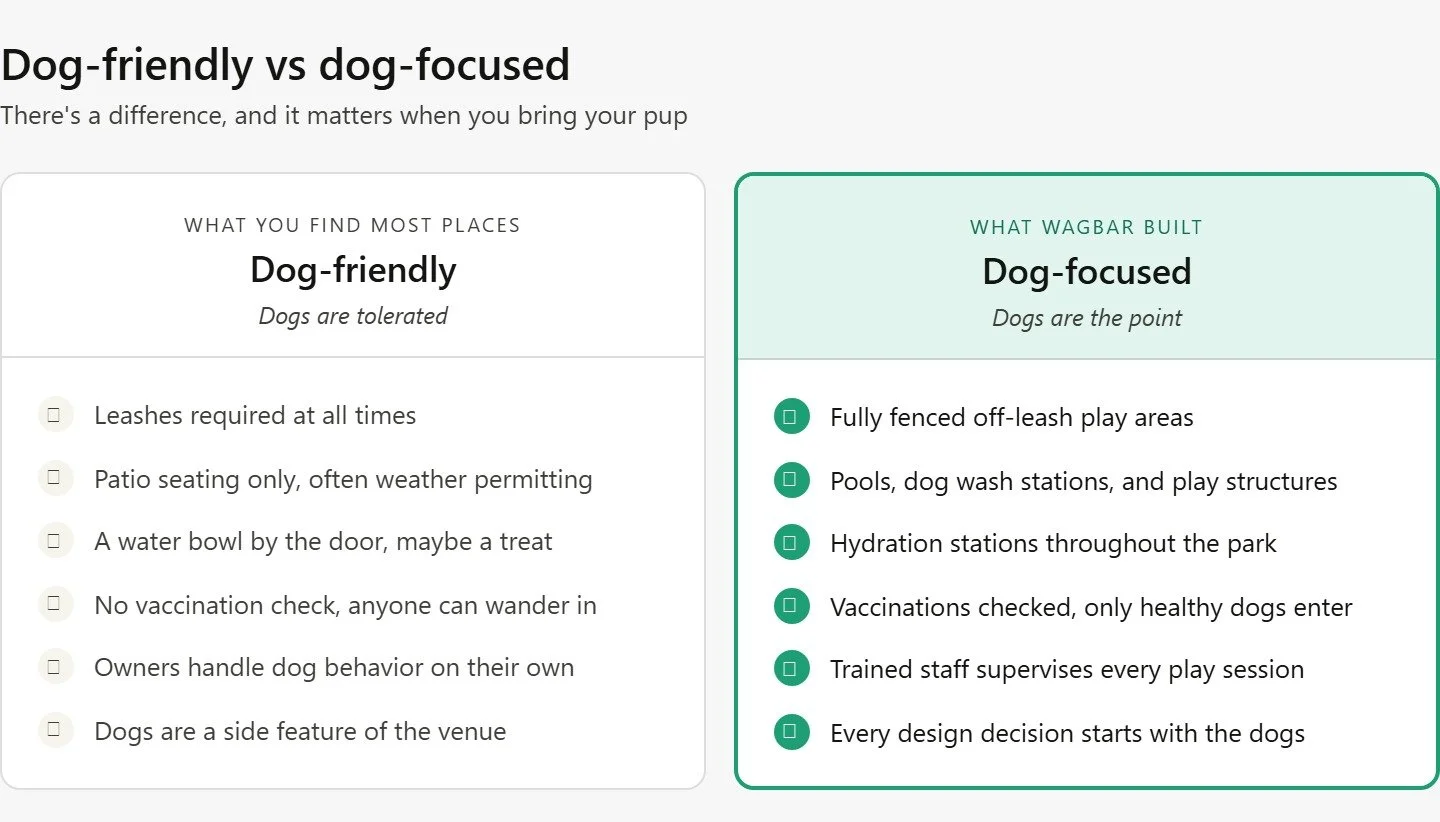

What Successful Dog Park Bars Have in Common

The operators that are growing tend to share a specific set of characteristics. None of these are complicated, but together they create a model that's more resilient than the high-overhead alternatives.

Low Fixed Costs and Simple Operations

The most successful dog park bars run lean. They serve drinks, not dinner. They partner with food trucks rather than running kitchens. They use modular or prefabricated structures for the bar itself, which dramatically reduces buildout costs and timelines.

Wagbar's container bar system is a good example. The bar arrives substantially pre-built, which cuts construction time and contractor costs. MUTTS uses a similar approach with prefabricated 1,100-square-foot cantina structures that can be assembled in 10 to 12 weeks. This isn't just a cost play. It's an operational simplification that keeps the staff focused on the two things that actually matter: keeping dogs safe and pouring good drinks.

Recurring Membership Revenue

The membership vs. day pass revenue model is the financial backbone of the category. Dog park bars that build a strong membership base create predictable monthly revenue that covers fixed costs regardless of weather, season, or foot traffic on any given day.

Most successful operators offer tiered pricing: day passes for visitors and tourists, monthly memberships for regular locals, and annual memberships at a discount for committed members. The key metric is membership retention rate. Venues with strong community programming (trivia nights, breed meetups, live music, seasonal events) tend to retain members longer because the dog park bar becomes a weekly habit, not just an occasional outing.

Beverage-Focused Revenue

Bar revenue on a per-visit basis is where dog park bars make their margin. A customer who comes in with a $10 day pass and buys two $7 craft beers has generated $24 in a single visit. Multiply that across weekday evenings and packed weekend afternoons and the numbers work.

The drink menu doesn't need to be extensive. Local craft beer on draft, a selection of canned options, wine, hard seltzer, and a few cocktails covers the full range of customer preferences. Hot drinks and non-alcoholic options matter more than people think because they keep dog owners coming even when they're not in the mood for alcohol. The complete guide to off-leash dog bar licensing covers the regulatory side of beverage service, which varies meaningfully by state.

Community Building as a Business Strategy

This is the part that separates a good dog park bar from a great one. The venues that thrive don't just provide a space for dogs to play. They create a community that people want to belong to.

That means regular events: weekly trivia, monthly breed meetups, holiday celebrations, live music, adoption events with local rescues. It means staff who know the regulars and their dogs by name. It means a social media presence that features the community, not just the brand.

Wagbar's Asheville flagship is a case study in community-driven success. It's been voted Best Pet Friendly Bar/Brewery at the Best of WNC Mountain Express awards multiple years running and landed on USA Today's 10Best Dog Bars list. That kind of recognition comes from the community, not from marketing spend. The social impact of dog-centric venues is real and measurable in retention rates, word-of-mouth referrals, and local media coverage.

Professional Dog Supervision

Every successful dog park bar employs staff specifically trained in dog behavior and group play dynamics. This is the single biggest differentiator from free public dog parks, where supervision is the owner's responsibility and incidents are common.

Trained staff monitor play continuously. They recognize warning signs before fights escalate. They enforce vaccination requirements and behavioral standards. They create the safe environment that justifies a membership fee and builds the trust that brings families back week after week. Venues that underinvest in this area, treating it as a cost center rather than a core feature, tend to have more incidents and worse retention.

Revenue Benchmarks and Unit Economics

Hard financial data on dog park bars is scarce because most operators are privately held and don't publish financials. But we can assemble a reasonable picture from franchise disclosure documents, industry reporting, and what operators have shared publicly.

Startup investment ranges vary significantly by model. Wagbar's franchise investment runs from approximately $470,000 to $1.1 million total, including a $50,000 franchise fee. MUTTS Canine Cantina's estimated initial investment ranges from $1.4 million to $1.7 million with a $40,000 franchise fee. Independent operators building from scratch can fall anywhere in that range depending on land costs, construction, and local permitting. The complete breakdown of startup costs offers a framework for thinking through these numbers.

Revenue streams typically break down into three to four categories:

Membership and day pass fees typically represent 30% to 50% of total revenue. This is the most predictable stream and the foundation that covers base operating costs.

Bar and beverage sales usually account for 35% to 50% of revenue. This is where the margin lives. Beverage cost of goods is typically 20% to 30%, which is favorable compared to food-heavy models.

Events, private parties, and merchandise fill in another 10% to 20%. Private event rentals can be especially lucrative on weekday evenings and weekend mornings when regular traffic is lighter.

Food truck partnerships generate modest revenue through either flat fees or percentage arrangements but more importantly keep customers on-site longer and increase bar spend per visit.

Labor costs are the biggest ongoing expense. Dog park bars need bartenders and park monitors at minimum. The staffing requirements for dog park operations include people who can both serve drinks and manage dogs safely, which is a specific skill set that not every hospitality worker possesses.

Seasonality matters. Dog park bars in the Southeast, Sun Belt, and West Coast enjoy year-round operation. Venues in northern climates face reduced traffic in winter, which operators offset with heaters, covered areas, indoor spaces, hot beverages, and event programming. The Wagbar locations tracker shows a deliberate expansion pattern favoring markets with longer outdoor seasons.

Regional Expansion Patterns and Where the White Space Is

Dog park bars are not evenly distributed. The current concentration patterns reveal both where the concept works best and where the biggest growth opportunities exist.

Where Dog Park Bars Are Concentrated

Texas leads the country in dog park bar density. MUTTS has multiple locations in DFW. Yard Bar operates in Austin. BARk House Social just opened in East Austin. The combination of warm weather, outdoor culture, high dog ownership, and relatively affordable commercial real estate makes Texas a natural hub.

The Southeast is the second strongest region. Wagbar's flagship and franchise expansion are anchored here, with locations in Asheville, Knoxville, and franchise territories across the Carolinas, Georgia, and Virginia. Fetch Park has multiple locations in the Atlanta metro. The Southeast benefits from relatively long outdoor seasons, growing metros, and strong dog ownership rates.

Florida has several independent operators including Pups Pub (Orlando and Tampa) and The Dog Bar (St. Petersburg). The year-round warm weather is an obvious advantage, though summer heat requires shade infrastructure, misting systems, and pool features.

The Midwest is just starting. K9 Garden's opening in St. Louis, filling the space Bar K left behind, signals demand even after a high-profile failure. PG&J's in Louisville has built a strong following. Wagbar has a franchise territory in Cincinnati. But the Midwest remains under-served relative to population density and dog ownership.

The Northeast has the fewest dog park bars relative to its massive urban dog population. Park-9 Dog Bar in the Boston area and Dog Daze Social Club in DC are among the limited options. New York City, Philadelphia, and northern New Jersey represent enormous untapped markets. The challenge is real estate cost and availability, as the model requires significant outdoor square footage.

Where the White Space Exists

The largest gap is in major metros that don't yet have a dog park bar. Some specific opportunities:

Denver has Skiptown but could easily support multiple venues given its dog ownership rates and outdoor culture. Wagbar has identified Denver as a target market.

Nashville, Portland, San Diego, and Seattle all have the right combination of dog-friendly culture, craft beverage scenes, and young professional populations, but limited or no dog park bar options.

Suburban markets in major metros are another frontier. The first wave of dog park bars concentrated in urban cores. But dog ownership is even higher in suburbs, lot sizes are more available, and commercial rents are lower. Wagbar's best cities for dog franchise success analysis emphasizes communities with median household incomes above $75,000, pet ownership rates above the national average, and existing pet service infrastructure.

What's Next for the Dog Park Bar Industry

The next two to three years will determine whether dog park bars become a permanent fixture of American social life or remain a niche curiosity. Based on what's happening now, the former looks more likely.

Franchise Models Will Dominate Growth

Independent operators will continue opening, but the fastest growth will come through franchise systems that can replicate proven models across markets. Wagbar and MUTTS are the two most active franchise brands in the space. The franchise approach solves the hardest problems facing independent operators: site selection, buildout design, operational training, supply chain, and marketing systems. The complete guide to franchise ownership explains why this structure works particularly well for concepts with operational complexity.

The Full-Service Restaurant Model Will Keep Struggling

The evidence from Bar K and Off Leash suggests that combining a full-service restaurant with a dog park creates more problems than it solves. Expect the winning formula to remain drink-focused: a great bar program, food truck partnerships for variety, and maybe a limited snack menu. The comparison of outdoor vs. indoor dog business models explores this operational trade-off in detail.

Indoor/Outdoor Hybrid Venues Will Grow

Climate constraints limit the category in northern markets. The solution is hybrid venues with both indoor and outdoor play areas, climate control, and the ability to operate year-round. Park-9 in the Boston area already runs this model. Expect more purpose-built indoor/outdoor facilities as the concept moves north and west.

Technology Will Improve Operations

Digital check-in systems, vaccination record management, membership apps, and capacity monitoring tools are already in use at the better-run venues. As the category matures, technology will handle more of the administrative burden, allowing staff to focus on what matters: watching the dogs and serving the customers. Wagbar's proprietary "Opener" app for franchisee onboarding is one example of how technology is being purpose-built for this category.

The Category Will Get a Name Everyone Agrees On

Right now, the industry uses "dog park bar," "dog bar," "off-leash dog bar," "off-leash bar," "dog park and bar," and half a dozen other variations interchangeably. As the category matures and media coverage increases, a standard term will emerge. The search data suggests "dog park bar" is winning, but "dog bar" runs a close second. Either way, the category is moving from "interesting concept" to "established industry segment" in real time.

The rise of the experience economy and the continued growth of pet spending suggest the tailwinds behind this category aren't going away. The question isn't whether dog park bars will keep growing. It's which operators will build the businesses that last.

Frequently Asked Questions About the Dog Park Bar Industry

How many dog park bars are there in the United States?

As of mid-2026, we estimate 60 to 70 dog park bars are currently operating in the US. This includes independent single-location operators, multi-unit brands like MUTTS Canine Cantina and Fetch Park, and franchise locations from brands like Wagbar. The number is growing by roughly one to two new openings per month.

Why did Bar K close?

Bar K permanently closed all three locations (Kansas City, St. Louis, and Oklahoma City) in July 2025. The company cited severe economic challenges including inflation, rising labor costs, reduced consumer spending, and location-specific problems. The Kansas City location was impacted by construction that limited access and parking. The St. Louis location had faced a $298,000 unpaid rent lawsuit.

How much does it cost to open a dog park bar?

Investment ranges vary by model. Wagbar franchise locations require an estimated total investment of $470,000 to $1.1 million. MUTTS Canine Cantina franchises range from $1.4 million to $1.7 million. Independent operators can fall anywhere in that range depending on land, construction, and local requirements. The biggest variable is whether the model includes a full-service kitchen, which adds significant cost and complexity.

Are dog park bars profitable?

The operators that run lean, beverage-focused models with strong membership bases report healthy margins. Profit margins for dog business franchises depend on location, membership volume, bar revenue per customer, and labor efficiency. Venues that avoid full-service kitchens and maintain high membership retention tend to perform best. Venues that over-invest in food service or expand too quickly face higher risk of financial strain.

What's the difference between a dog park bar and a dog-friendly bar?

A dog park bar has a fenced, supervised off-leash play area where dogs can run freely. Dogs typically need vaccinations and a membership or day pass. A dog-friendly bar is a regular bar that allows dogs on a leash, usually on an outdoor patio. The experiences are fundamentally different in terms of what the dog gets out of it.

Which dog park bar franchise brands are currently expanding?

The two most active franchise brands are Wagbar, with 16+ territories sold and locations operating in Asheville, NC and Knoxville, TN, and MUTTS Canine Cantina, with locations in Texas and franchise development in Arizona, Colorado, and Kansas. Both brands are actively seeking franchisees in new markets.

Where are dog park bars most popular?

Texas and the Southeast US have the highest concentration. Florida, the Midwest, and California are growing. The Northeast remains significantly under-served despite having massive urban dog populations. Markets with high dog ownership, outdoor social culture, and craft beverage scenes tend to support dog park bars well.

What makes Wagbar's model different from other dog park bar brands?

Wagbar uses a container bar system that arrives substantially pre-built, reducing construction costs and timelines. The model is beverage-focused without a full-service kitchen, which simplifies operations. Franchisees receive training at the Asheville headquarters, on-site opening support, and ongoing business reviews. The concept was proven over five-plus years at the flagship location before franchise expansion began.

Meta Description: The dog park bar industry has grown to 60+ US venues in 2026. See which models are working, why Bar K closed, and where the category is headed next.

Bottom TLDR: The dog park bar industry is growing steadily alongside a $158 billion US pet economy, with new venues opening monthly and franchise brands like Wagbar expanding into 16+ markets. The operators succeeding in 2026 share a clear pattern: low-overhead buildouts, drink-focused menus, recurring membership revenue, and genuine community ties. Explore Wagbar's franchise opportunity or find your nearest location to see the model in action.