Pet Industry Growth and the Off-Leash Dog Bar Boom: 2025-2030 Category Outlook

Top TLDR: Pet industry growth and the off-leash dog bar boom are running on the same demographic engine: roughly two of every three U.S. households own a pet, total pet spending crossed $147 billion in recent estimates, and the experience-economy share keeps rising. The off-leash dog bar category went from a handful of operators in 2019 to multi-state franchise systems by 2025. Operators evaluating the 2025-2030 window should target mid-sized cities with strong existing experience economies.

The pet industry is one of the most reliable growth stories in U.S. consumer spending. The American Pet Products Association reports that 67% of households own a pet, dogs are the most common species, and total spending has climbed from roughly $103 billion in 2020 to estimates above $147 billion in recent years, with longer-range projections pointing toward $261 billion by 2030 across some forecast models. That growth pattern matters not just for the category as a whole but for the specific corner of it where dogs and hospitality meet, including the off-leash dog bar concept that has spread fast since the late 2010s.

This page lays out where the pet industry sits today, how the off-leash dog bar boom is positioned inside that broader market, and what the 2025-2030 window looks like for operators planning new locations. The argument is that the category is still early enough in its growth curve to favor first movers in untapped markets, but mature enough that operating standards, franchise systems, and customer expectations are now well defined. The deeper pet industry market analysis gives the full breakdown of how spending is distributed across categories.

What the Pet Industry Looks Like Heading Into 2025

Pet spending in the United States has roughly doubled in nominal terms over the past decade. The category was around $70 billion in 2014, passed $103 billion in 2020, and reached estimates above $147 billion in more recent surveys. Spending has continued to grow even through inflation cycles and economic uncertainty, which is one reason analysts treat pet-related categories as relatively recession-resistant. A 2023 Pew Research Center survey found that 97% of pet owners consider their pets' emotional well-being a top priority, which helps explain why discretionary pet spending tends to hold up better than other discretionary categories.

The composition of that spending has shifted as well. Food and veterinary care still dominate the totals, but services and experiences are the fastest-growing segments. Day care, training, dog walking, grooming, pet insurance, and now experience-based venues such as dog cafés, dog yoga studios, and off-leash dog bars all sit in the services bucket. The detailed pet industry growth trends through 2030 show services growing faster than goods on a percentage basis across most forecasts.

Demographic tailwinds are strong heading into the second half of the decade. Younger consumers, including millennials and Gen Z, own pets at higher rates than older generations did at the same age. Many of these owners are urban or first-ring suburban, do not have children, and treat the dog as the primary household companion. That demographic profile lines up almost perfectly with the customer base off-leash dog bars are designed to serve.

How the Off-Leash Dog Bar Boom Fits the Numbers

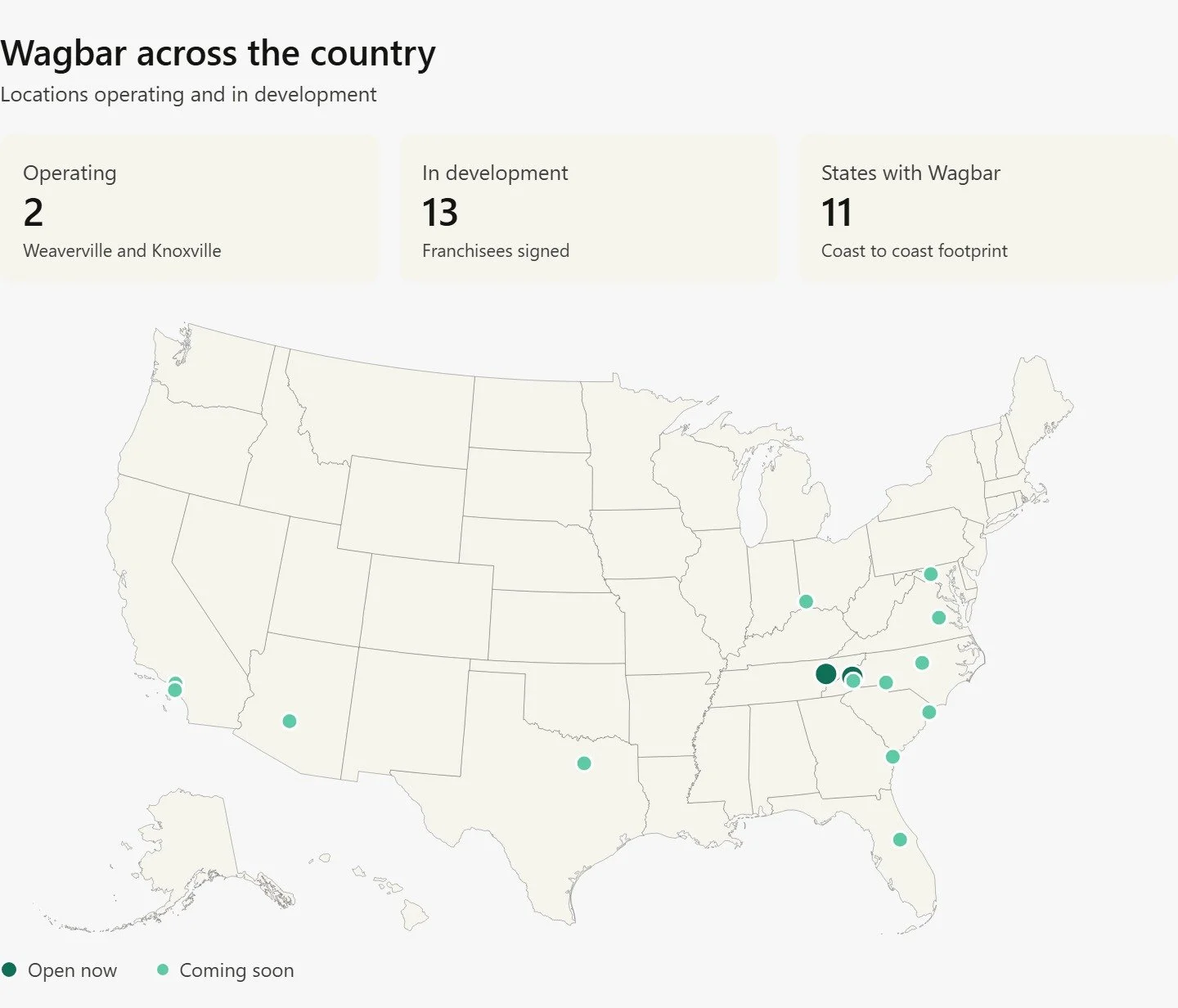

The off-leash dog bar category is small in absolute terms but is one of the fastest-growing segments inside the broader pet services category. Wagbar opened in Weaverville, just north of Asheville, in November 2019 with a single location. By 2025, the brand has more than a dozen sites in operation or development across ten states, with confirmed franchisees in markets including Richmond, Phoenix, Los Angeles, Knoxville, Charlotte, and Myrtle Beach. The Knoxville site, opening at the former Creekside Knox property, represents the second open Wagbar after Weaverville.

USA Today's 10Best list named Wagbar the #10 Best Dog Bar in 2024, the same year the publication began running a national category list at all. A national paper running a "best of" list in a category is, by itself, evidence that the category exists in the public mind. Five years earlier, that list could not have run because there were not enough credible nominees. The fact that a list now exists, and that an operator like Wagbar can place on it without buying advertising, signals where the category sits on its growth curve. The community-building playbook for dog-focused businesses describes the operating discipline that is becoming standard across early operators.

Other independent operators in cities such as Austin, Charlotte, Tampa, and Raleigh have been working on similar concepts in parallel. Most are single-unit operations, but some are starting to add second locations or convert into franchise systems. The pattern resembles the early years of the craft brewery boom in the late 2000s, where independents and small chains coexisted before consolidation began.

Why the 2025-2030 Window Looks Favorable

Three conditions usually have to line up for a new hospitality category to enjoy a strong five-year window: durable demand, untapped geography, and emerging operating standards. All three are visible in the off-leash dog bar category right now.

Durable demand comes from the underlying pet ownership numbers and the experience-economy shift. Pet ownership rates have been stable in the high 60s for years and show no sign of dropping. Experience spending continues to take share from goods spending. Younger consumers, who are now in their prime household-formation years, are more likely to own pets and more likely to choose experience venues than older generations did at the same age.

Untapped geography is the clearest opportunity. Most U.S. metro areas of 250,000 to 750,000 residents do not yet have an off-leash dog bar, and many do not have one within a comfortable drive. Wagbar's pipeline targets exactly this band: Richmond, Knoxville, Cary, Charlotte, Myrtle Beach, Savannah, Frederick, Cincinnati, Phoenix, and parts of greater Los Angeles. The geographic pattern documented in where dog franchise concepts succeed lines up with cities that already have high dog ownership rates and active craft-beverage cultures, which is the same demographic and lifestyle profile that produced the early independents.

Emerging operating standards are the third piece. By 2025, the category has roughly converged on a set of practices: vaccination intake at first visit (Rabies, Bordetella, Distemper at minimum), minimum age and spay or neuter requirements, supervised play areas, free entry for human guests aged 18 and older, membership tiers built around weekly return visits, and rotating food trucks rather than fixed kitchens. New entrants do not have to invent these practices anymore; they can adopt the playbook and put their effort into location, programming, and community building instead.

What the Category Looks Like at Maturity

Most maturing experience-economy categories settle at a few hundred operators nationwide and a small number of multi-unit franchise systems. Craft breweries, axe-throwing bars, escape rooms, and self-pour taprooms each followed similar arcs. The off-leash dog bar category is on track to reach a similar profile by the end of the decade, assuming current growth rates hold.

A useful rough estimate: if 5% of U.S. metro areas with 250,000 or more residents eventually support at least one off-leash dog bar, the category would have roughly 75 to 100 metro markets covered. Each metro could plausibly support one to three locations, with the largest cities supporting more. That math suggests a national field of 200 to 400 venues at maturity, which is consistent with how craft breweries grew during their own peak window.

Wagbar's franchise economics give a sense of what a multi-unit operator could expect. Published initial investment ranges from $470,300 to $1,145,900 per location, with a $50,000 franchise fee, a 6% royalty on adjusted gross sales, and a 1% marketing fund contribution. Multi-unit commitments of three or more locations qualify for a 50% franchise fee discount. Those numbers sit within the normal small-format hospitality range and have already attracted operators from finance, IT, corporate, and restaurant backgrounds. Profile examples appear in dog business franchise profit margins and real owner stories.

Risks and Friction Points to Watch

The 2025-2030 outlook is not entirely clear. Three issues are worth tracking. The first is weather. Most early operators launched in mild Sun Belt or mountain markets where outdoor operation works year-round. Colder markets such as Cincinnati, Frederick, and parts of the Midwest are still proving out the format. Operators in those markets are testing covered patios, partial enclosures, heaters, and shipping-container bar structures. Wagbar's container bar build-out, developed with a manufacturing partner, is one example of a standardization aimed at reducing build time and improving cold-weather performance.

The second is local zoning and licensing. Off-leash dog bars sit at the intersection of food-service liquor licensing, animal-handling regulations, and outdoor venue zoning, all of which vary by city and state. California requires specific franchise pre-sale notice language. Oregon requires pre-sale registration as a process step. Texas is a non-registration state but has its own patio-only alcohol rules in cities such as Dallas. Operators planning expansion need to budget time for jurisdiction-specific approvals rather than assuming uniform rules.

The third is saturation in early markets. Asheville, Austin, and parts of California already have multiple operators competing for the same dog-owning customer base. New entrants in these markets need a clear differentiator on location, programming, or membership tiers rather than relying on category novelty. The catch-up windows in mid-sized markets are still wide open, but the original-market windows are starting to close. The current Wagbar locations roster shows where the brand has already committed and where regional clusters are forming.

What This Means for Aspiring Operators

Operators planning to enter the category between 2025 and 2030 should think about market choice, format choice, and timing in that order. Market choice is the most important variable: a strong concept in a weak market struggles, while a competent operator in a strong market usually does well. The strongest near-term targets are mid-sized metros with high dog ownership rates, active craft-beverage cultures, mild-to-moderate climates, and minimal existing competition.

Format choice covers the build-out decisions that define the venue. Most operators choose between an outdoor-first venue with a container bar and a renovated existing structure. The container approach standardizes the build, holds down costs, and ships faster; the renovation approach can produce a more distinctive venue but often comes with surprise costs. Wagbar's flagship in Weaverville uses the container approach, and the model has carried over to most of the brand's locations in development.

Why Timing Matters for First Movers

Experience-economy categories are sensitive to local first-mover dynamics. The first off-leash dog bar in a 500,000-resident market typically captures a strong regular base before competitors enter. Waiting another two or three years often means watching that customer base pick a different operator, since the regulars who form the venue's core social fabric tend to stay loyal once they have built relationships with the staff and other dogs.

The full set of Wagbar franchise opportunities lays out what the support model looks like for operators who want to move faster than they could with a from-scratch build. Container bar standardization, the proprietary Opener pre-opening app, one-week training in Asheville, and on-site grand-opening support all compress the timeline between signing and opening day.

Frequently Asked Questions

How big is the U.S. pet industry today?

Total U.S. pet spending was around $103 billion in 2020 and has grown to estimates above $147 billion in more recent surveys. The 2030 outlook ranges across forecasters but $261 billion is one widely cited projection. Pet ownership has held steady at roughly 67% of U.S. households across multiple survey waves, with dogs as the most common species.

Where does the off-leash dog bar category fit inside that?

The off-leash dog bar category is part of the pet services bucket, which is the fastest-growing segment of overall pet spending. The category is small in absolute dollars compared to food, vet care, or grooming, but it is growing faster on a percentage basis. National recognition such as USA Today's 10Best Dog Bars list signals that the category has crossed into mainstream consumer awareness.

How many off-leash dog bars exist now and how many will exist by 2030?

Exact counts are imprecise because the category has no central registry. Several dozen are operating across the United States as of 2025, with growth concentrated in Sun Belt and mountain-west markets. A reasonable rough projection puts the category at 200 to 400 venues nationwide by the end of the decade, assuming current growth rates and franchise expansion continue.

Which markets are still open?

Mid-sized metros with 250,000 to 750,000 residents are the largest white space. Cities with high dog ownership, active craft-beverage cultures, and mild-to-moderate climates are the strongest near-term targets. Wagbar's pipeline covers many of these markets directly, including Richmond, Phoenix, Knoxville, and Charlotte, but plenty of comparable cities still have no operator. The Knoxville location at the former Creekside property is a current example of how a second-tier city can host a strong second-flagship venue.

What is the typical investment to open one?

Wagbar's published initial investment range is $470,300 to $1,145,900 per location, including a $50,000 franchise fee, a 6% royalty on adjusted gross sales, and a 1% marketing fund contribution. Multi-unit commitments of three or more locations qualify for a 50% franchise fee discount. Independent operators outside the franchise system typically face similar build-out costs but without the support, training, and brand backing that the franchise model includes.

Bottom TLDR

Pet industry growth and the off-leash dog bar boom should keep moving together through 2025-2030, supported by stable pet ownership rates, rising experience spending, and a pipeline of mid-sized cities still without operators. National recognition from USA Today's 10Best and franchise expansion across ten states signal the category has cleared early-stage adoption. Operators planning new locations should target mid-sized metros with strong existing experience economies before the first-mover windows close.