How the $261 Billion Pet Industry Became a Recession-Resistant Business Category

Top TLDR

The $261 billion pet industry is one of the few consumer categories that has grown through every U.S. recession since the 1990s, driven by the emotional bond between owners and their animals. Americans consistently prioritize spending on their pets even when cutting back elsewhere, making pet businesses structurally more stable than most discretionary categories. If you're evaluating a pet business investment, understanding why this industry holds up in downturns is the right place to start.

Most consumer categories contract when the economy tightens. Pet spending does not. During the 2008 financial crisis, U.S. pet industry revenue grew 5.1% while overall retail sales dropped sharply. During the early months of the COVID-19 recession in 2020, pet adoptions surged and annual industry spending crossed $103 billion for the first time. By 2023, the American Pet Products Association reported U.S. pet spending had reached $147 billion.

The $261 billion figure reflects global projections for the pet industry through 2030, based on compound annual growth rates tracked by multiple market research firms. That number gets cited frequently, and for good reason: it signals that the structural demand driving pet spending has room to grow well beyond where it stands today.

Understanding why this industry holds up the way it does matters if you're thinking about investing in a pet business, franchising in the pet space, or trying to evaluate which pet service categories are better positioned than others.

What "Recession-Resistant" Actually Means

Recession-resistant does not mean immune to economic pressure. It means a category shows meaningfully lower revenue decline during downturns compared to the broader economy, and recovers faster when conditions improve.

Pet spending fits that definition because of a single underlying factor: owners treat their animals as family members. According to the American Pet Products Association, approximately 67% of U.S. households owned a pet as of 2023. The Human Animal Bond Research Institute found that 85% of pet owners consider their pets part of the family. When household budgets tighten, people cut vacations, restaurant spending, and clothing budgets. They do not typically cut spending on food, basic care, or comfort for an animal they think of as a member of the household.

This "pet humanization" trend has been documented consistently since at least 2010 and has accelerated among millennial and Gen Z pet owners, demographics now representing the majority of first-time pet buyers. These cohorts spend more per pet than prior generations and are more likely to seek premium options across food, health care, and services.

The result is a category with what economists call inelastic demand. Price increases and income drops produce less behavior change than they would in discretionary spending categories like entertainment or home furnishings.

How the Industry Got to $261 Billion

The American Pet Products Association tracked roughly $17 billion in U.S. pet industry spending in 1994. Thirty years later, that number had grown nearly ninefold. Understanding the categories driving that growth clarifies where the durable opportunity lies.

Pet food and treats remain the largest segment, accounting for roughly $65 billion in U.S. spending alone as of 2023. Growth here has been driven by premiumization: owners trading up to grain-free formulas, raw diets, and species-appropriate nutrition. This segment is mature but still growing.

Veterinary care and products crossed $38 billion in 2023 and continue climbing alongside pet insurance adoption and advances in veterinary medicine. Owners who view their pets as family members are willing to pursue diagnostics, surgeries, and specialist care that would have been unusual a generation ago.

Pet services represent the fastest-growing segment on a percentage basis. This includes grooming, boarding, training, day care, and newer experience-based categories like off-leash dog park bars. Services are where the structural growth story gets most interesting from an investment standpoint, because service businesses can't be displaced by e-commerce, they're locally anchored, and the best ones build membership communities that reduce churn.

The global projection to $261 billion by 2030 is largely driven by international market expansion, particularly in Asia, where pet ownership rates are rising rapidly from a lower base, and continued premiumization in established markets like the U.S., Western Europe, and Australia.

Why Service Businesses Outperform During Downturns

Not all pet businesses are equally recession-resistant. Product margins compress when input costs rise. Veterinary care faces cost pressure as technology advances. But service businesses built around recurring membership models have shown particular durability.

The mechanism is straightforward. A pet owner who pays a monthly or annual membership to a dog park or daycare has pre-committed their spending for that period. They've already decided the service is worth the cost. During an economic downturn, they're more likely to cut one-time discretionary purchases than cancel a recurring membership that their dog (and their own social life, in the case of a venue like Wagbar) depends on.

This is part of why pet industry market analysis consistently shows services outperforming products during periods of economic contraction. Products face direct price competition and are subject to trading down. Services with strong community attachment are stickier.

The off-leash dog bar model sits at the premium end of the service market, but it also captures a consumer behavior that has proven durable: the combination of off-leash dog time and social space for owners. That dual value proposition, something for the dog and something for the owner, is harder to give up than a product that could be swapped for a generic alternative.

What Drove the Post-2020 Pet Spending Surge

The 2020 to 2023 period saw acceleration that deserves specific attention because it permanently expanded the pet owner base.

During the lockdown period of early 2020, animal shelters reported adoption surges of 30% to 40% in many markets. The American Pet Products Association reported approximately 23 million U.S. households acquired a new pet between 2020 and 2021. Many of these were first-time pet owners, and a disproportionate share were millennials and younger adults working from home.

These new pet owners then spent at rates that surprised even industry analysts. They invested heavily in premium food, veterinary wellness plans, training, and services designed to provide mental stimulation for pets living in smaller spaces. They also had dogs during a period when human social spaces were limited, which deepened the emotional bond in ways that typical pet owners experience over longer time periods.

By 2022 and into 2023, this expanded owner base was spending its way into the full range of pet industry opportunities. The $147 billion in 2023 U.S. spending represents the baseline that analysts use when projecting toward the global $261 billion figure by 2030.

Regional Patterns and Where Growth Concentrates

Pet spending isn't uniform across the country. Regional pet spending patterns show significant variance by metro area, state, and demographic composition.

Higher-income metros with large millennial homeowner populations and strong outdoor and wellness cultures tend to produce the highest per-pet spending. Cities like Asheville, Denver, Austin, Nashville, and Richmond consistently rank above the national average on both pet ownership rates and per-pet service spending.

This geographic pattern matters for anyone evaluating a pet franchise opportunity. A market with strong demographic alignment, including college-educated households, higher disposable incomes, and an established culture of spending on local experiences, will support a premium pet service business more reliably than a market where those factors are absent.

The concentration of pet spending demographics in specific metro areas isn't accidental. It reflects the intersection of income, cultural values around pet ownership, and infrastructure investment in pet-friendly spaces. Markets that have invested in dog parks, pet-friendly restaurants and bars, and dog-friendly housing tend to attract more pet owners, which drives more spending, which supports more pet businesses.

The Competitive Structure of the Pet Services Market

The pet services market is fragmented compared to pet food and veterinary care, which have large national players. Independent groomers, trainers, boarding facilities, and day cares still dominate in most markets, which creates an opportunity for franchise concepts that can provide consistent brand identity, training, and operational systems.

Pet industry competitive analysis shows that the franchise segment of pet services has been growing faster than independent operators over the past decade, driven by consumer preference for predictable quality and brand recognition. Franchises like Wagbar benefit from an established operational model, a known safety protocol, and a brand that communicates premium experience before a new customer ever walks through the gate.

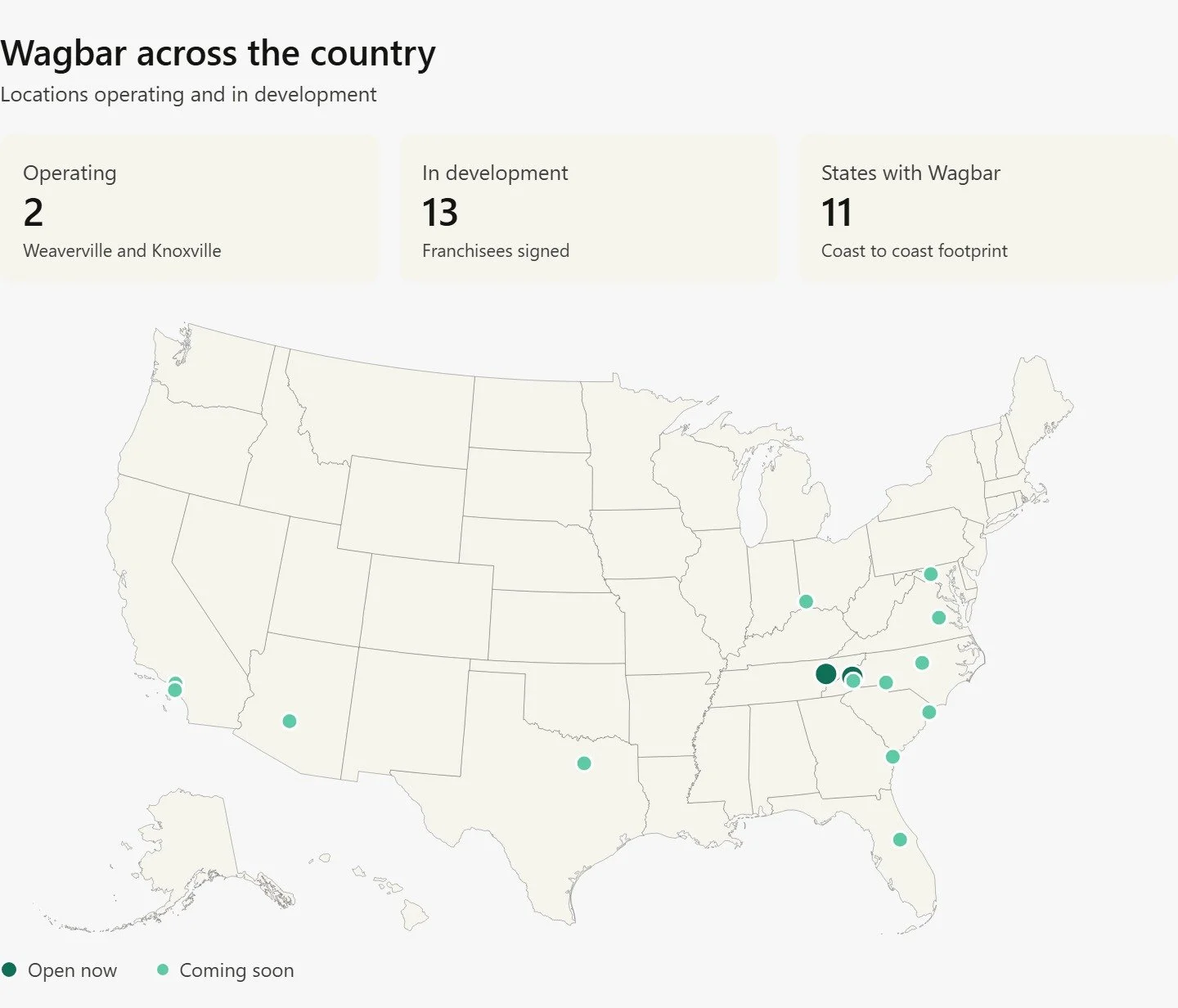

The off-leash dog bar category specifically has low competition at the franchise level. The concept is proven in markets like Asheville and Knoxville, but the national footprint is still in early development, which means entry points exist in markets where the concept hasn't yet been established.

For investors evaluating types of animal franchise opportunities across the industry, the fragmentation of the service segment is actually a favorable signal. In a fragmented market with demonstrated consumer demand, a well-executed franchise has more room to establish category dominance in a given geography than it would in a market with several entrenched national competitors.

What the $261 Billion Projection Means for Franchise Investors

Global projections carry uncertainty, and they should always be evaluated alongside more granular market data. But the structural forces behind the pet industry's trajectory are concrete: demographic momentum from millennial pet owners, geographic expansion of international markets, continued premiumization across food and services, and the deepening human-animal bond that sustains spending through economic cycles.

For franchise investors, the more practically relevant number is the local market opportunity. A market with 500,000 dog-owning households, an above-average household income, and no existing off-leash dog bar concept represents a quantifiable opportunity independent of what the global market does by 2030.

Wagbar's initial franchise investment ranges from $470,300 to $1,145,900 (see the Franchise Disclosure Document for detailed financial performance figures). The franchise fee is $50,000, with a 6% royalty on adjusted gross sales and 1% to the marketing fund. Multi-unit operators committing to three or more units qualify for a 50% discount on the franchise fee.

The investment enters a market category with a documented history of holding up during downturns, recurring membership revenue on the dog park side, and beverage revenue on the bar side. That combination of structural resilience and dual revenue streams is what makes the pet industry's recession-resistance relevant at the franchise investment level, not just at the macro level.

Frequently Asked Questions

Why is the pet industry considered recession-resistant?

Pet owners treat their animals as family members and consistently prioritize pet spending over other discretionary categories when budgets tighten. During the 2008 recession and the 2020 economic contraction, U.S. pet industry spending grew rather than declined, driven by inelastic demand for food, basic care, and services tied to emotional attachment.

What is the $261 billion pet industry figure based on?

It represents global pet industry revenue projections through 2030, derived from compound annual growth rates tracked by multiple market research firms. The figure includes pet food, veterinary care, services, and supplies across North America, Europe, Asia, and other expanding markets.

Which segments of the pet industry are growing fastest?

Pet services, including grooming, boarding, training, and experience-based venues, are growing fastest on a percentage basis. Pet food remains the largest absolute segment but is more mature. Veterinary care and pet health technology are also growing steadily with rising insurance adoption and advances in medical treatment.

How did COVID-19 affect pet industry spending?

The pandemic period significantly expanded the pet owner base. Approximately 23 million U.S. households acquired a new pet between 2020 and 2021. These new owners spent at above-average rates on premium food, training, and services, pushing U.S. annual pet spending from roughly $103 billion in 2020 to $147 billion by 2023.

Do pet franchise businesses perform better than independent pet businesses?

Franchise models have grown faster than independent operators in the pet services segment over the past decade, driven by brand recognition, consistent quality standards, and operational support systems that reduce the learning curve for new business owners. Franchise affiliation can also provide marketing and technology infrastructure that independent operators would need to build from scratch.

What makes an off-leash dog bar more recession-resistant than other pet businesses?

The combination of a membership model and dual revenue streams from park access and bar sales provides more financial stability than a single-service format. Membership pre-commitment means revenue is partially locked in regardless of visit frequency. The social community that builds around a regular venue also creates retention that's harder to break than a transactional relationship.

A Category Built for the Long Run

The $261 billion pet industry didn't get there by accident, and it hasn't maintained its trajectory through multiple economic cycles by luck. The emotional foundation of pet ownership creates a spending pattern that holds up when other consumer categories contract.

For investors evaluating this space, the relevant question isn't whether the industry is growing. It clearly is. The question is where within the industry the most durable business models sit. Experience-based service businesses with membership structures and community retention are well-positioned answers to that question.

If you're ready to evaluate a specific opportunity, explore Wagbar's pet franchise information and review the FDD for detailed figures on investment and financial performance.

Bottom TLDR

The $261 billion pet industry has grown through every U.S. recession since the 1990s because pet owners prioritize spending on their animals even when cutting elsewhere. The fastest-growing segment is pet services, particularly experience-based venues with membership models that create recurring revenue and community retention. To act on this, review pet franchise opportunities that combine dual revenue streams with the structural stability the industry has demonstrated historically.